Ein Unternehmensverkauf ist eine heikle Angelegenheit. Denn die Anzahl möglicher Fehlerquellen ist hoch. Eine falsche Unternehmensbewertung führt zu einem purchase price far too low or scare away all interested parties.

Besonders schlimme Auswirkungen kann die Weitergabe von Firmeninternas an Wettbewerber haben, die von einem Kaufinteressenten weitergegeben wurden. Um den Prozess des Unternehmensverkaufs zu verdeutlichen, werden im Folgenden die wichtigsten Schritte erläutert.

But before analysing, one point must be made: Every business sale is different. Daher sind viele Entscheidungen von der individuellen Situation abhängig. Denn zwischen einem Verkauf im Rahmen einer Altersnachfolge, einem Sanierungsverkauf oder einer vom Konkurrenten erzwungenen Firmenübernahme liegen Welten.

Sie haben nicht viel Zeit zu lesen? Hier der Unternehmensverkauf Ablauf in Kürze

In the preparatory phase of the sale of the company, the goals and the strategy to achieve them are determined. Here the especially the company valuation is important. Denn der Wert des Unternehmens entscheidet über den Kaufpreis.

In der Vermarktungsphase gilt es, die richtigen potenziellen Käufer zu identifizieren und anzusprechen. Diese Personengruppe sollte auf die Strategie für den Verkauf abgestimmt sein. Ebenso gilt es früh zu entscheiden, ob ein Bieterverfahren oder eine Einzelsuche umgesetzt werden soll.

In der Unternehmensprüfung (DD) und Verhandlung prüfen die Interessenten, welche Risiken sie mit dem Unternehmenskauf eingehen. Ausgehend vom Ergebnis dieser Prüfung wird ein finales Kaufangebot erstellt, über das verhandelt werden kann. Einigen sich beide Parteien, fließt das Resultat der Verhandlung in einen Unternehmenskaufvertrag.

Table of contents

- Preparation phase

- Käuferansprache und Vermarktungsphase

- Unternehmensprüfung und Verhandlung

- Contract and conclusion

Preparation phase

Im Ablauf eines Unternehmensverkaufs spielt bereits der erste Schritt der Vorbereitungsphase eine wichtige Rolle. Sie stellt eine entscheidende Basis für den Erfolg des gesamten Verkaufsprozesses dar.

Preparation of the sales documents

Professionelle Investoren erhalten viele verschiedene Kaufangebote und neigen bei unklarer Datenlage auch schnell dazu ein Angebot abzulehnen. Ein Verkäufer muss daher die kurze Aufmerksamkeit, die er in der Angebotsphase erhält, nutzen. Daher gilt es, die relevantesten Informationen über das Unternehmen and to create information documents from them.

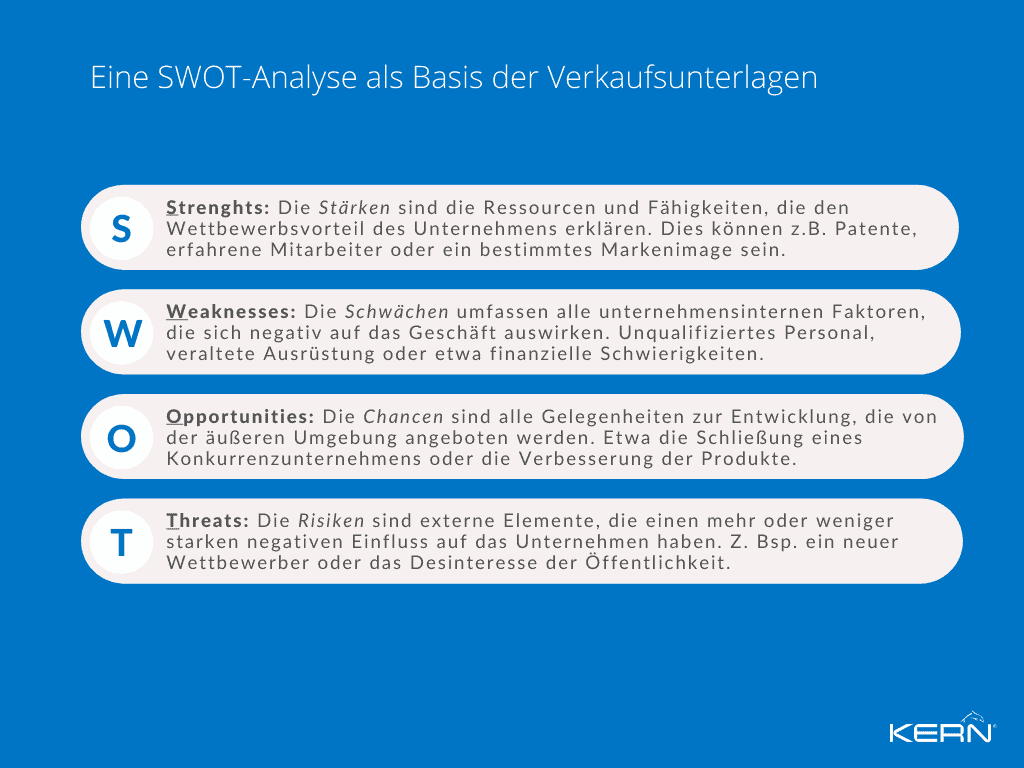

Der einfachste Weg, die Informationen aufzubereiten, ist die Auswertung interner Daten. Um die relevantesten Daten herauszufiltern, ist es wichtig, sich in den Käufer hineinzuversetzen. Welche Informationen steigern sein Interesse und sind für das Geschäftsmodell wirklich relevant? What is the USP (unique selling proposition) and what are the growth opportunities?

Auf jeden Fall sollte ein Käufer über die Stärken, Schwächen, Chancen und Risiken aufgeklärt werden. Daher kann eine SWOT-Analyse die Basis der Verkaufsunterlagen bilden.

M&A advice and tasks

Für viele Unternehmer stellt der Verkauf ihres Unternehmens einen einmaligen Vorgang dar. Allerdings steht dabei nicht nur viel Geld auf dem Spiel, sondern es gilt auch Haftungsrisiken zu minimieren. Daher suchen sich viele Unternehmer eine professional M&A consulting.

Diese Berater haben eine langjährige Erfahrung mit Corporate transactions und stehen dem Unternehmer mit ihrem Know-how zur Seite. Ihre Aufgaben reichen von der Ausrichtung der Verkaufsstrategie bis zur rechtlichen Prüfung des fertigen Kaufvertrags.

So werden Unternehmer nicht nur vor Fehlern bewahrt, die den Kaufpreis mindern könnten, sondern können über das Netzwerk der Berater eine Vielzahl interessierter Investoren in kürzester Zeit erreichen. Unabhängig davon, dass ein Projekt Company sale einen extrem hohen Zeitbedarf hat und dies über Berater intelligent komprimiert werden kann.

View verified purchase requests from entrepreneurs

M&A strategy

Um sich die richtige Strategie auswählen zu können, müssen die Ziele klar definiert sein. Die wichtigste Frage, die sich ein Unternehmer stellen sollte, lautet: Do I really want to sell 100% of the shares immediately or would I rather sell the shares step-by-step? And what do I want to sell? Je nachdem, wie diese Fragen beantwortet werden, kommen unterschiedliche Käufer infrage.

The company sale

Wenn ein Unternehmer nicht mehr direkt an seinem Unternehmen beteiligt sein möchte, bietet sich ein Verkauf zu 100 % an. Und zugleich ist ein Company sale not a blueprint.

Einige Investoren sind bereit, den Großteil und bis zu 100 % des Kaufpreises in Cash zu bezahlen, andere Investoren bevorzugen einen Kaufpreis, der sich an der zukünftigen Entwicklung des Unternehmens orientiert. Und die Parameter für einen Teil des Kaufpreises sind möglichst exakt und konkret mit allen Optionen schriftlich zu benennen.

Beide Seiten sollten früh klären, ob es eine Übergangsphase mit dem Verkäufer zur Einarbeitung geben wird und wie lang diese sein kann. Mehrheitlich muss der Verkäufer und abgebende Unternehmer einem Wettbewerbsverbot zustimmen. Manchmal werden sogar Familienmitglieder in dieses Wettbewerbsverbot mit integriert.

The company succession

At the Company succession fällt es vielen Firmeninhabern, die ein Unternehmen gegründet und aufgebaut haben, schwer zu akzeptieren, dass ihre Firma möglicherweise in der Zukunft mit einem anderen Unternehmen verschmolzen wird. Die Idealvorstellung der endlosen Fortführung der bisherigen Geschichte in die Zukunft steht unbewusst im Vordergrund.

Familienunternehmer sind eher auch bereit auf Geld zu verzichten, wenn das Unternehmen und die Mitarbeiter aus Ihrer Sicht in gute Hände kommen und der Übernehmer vermutlich mit einem hohen Verantwortungsbewusstsein zur Geschichte die Zukunft achtsam entwickeln wird.

Diese Wunschvorstellung eines Übergebers bzw. Verkäufers spielt auch bei einem innerfamiliären Generationswechsel eine Rolle. Meistens ist jedoch im Rahmen ähnlicher Wertvorstellungen und der gemeinsamen Vision der Generationen, diese wichtige Fragestellung für den Übergeber leichter zu klären und zu vertrauen.

Business valuation

The Business valuation ist eine subjektive Einschätzung über den Wert eines Unternehmens. Hierbei werden Modelle verwendet, die aus verschiedenen Unternehmensdaten einen „fairen“ Preis für ein Unternehmen ermitteln sollen.

The most important valuation methods in the purchase of a company are the discounted cash flow method, the capitalised earnings value method, the sub-total value method and the multiples method.

Bei der Discounted-Cashhflow- und der Ertragswertmethode werden die geschätzten zukünftigen Cashflows bzw. Jahresüberschüsse diskontiert und aufsummiert. Bei der Subtanzwertmethode wird der Wert aller Vermögensgegenstände geschätzt (ist bei Geschäftsmodellen sinnvoll, bei denen das Anlagevermögen wertvoller ist als der Ertrag).

Bei der Multiplikatoren-Methode werden Unternehmenskennzahlen wie Eigenkapital, Umsatz oder Gewinn mit gängigen Werten multipliziert, um eine grobe Schätzung des Unternehmenswerts zu erhalten. Das vereinfachte, steuerliche Ertragswertverfahren, eignet sich dagegen nicht, denn es setzt in der Regel deutlich zu hohe Faktoren ein. Aus der Sicht der Finanzbehörden logisch und gleichwohl entspricht es nicht dem üblichen Marktwert.

Can the value of the company be increased?

Unabhängig von Wahlmöglichkeiten im Handelsrecht zur bilanziellen Bewertung, sollte bei ausreichender Zeit des Verkäufers, jedes Geschäftsmodell eingehend auf Entwicklungspotentiale geprüft werden. Der „Tunnelblick“ verstellt nach vielen Jahren des Unternehmertums häufiger gewichtige Chancen für neue Märkte, Produkte, Dienstleistungen oder Skalierungen.

Heute gibt es in Verbindung mit künstlicher Intelligenz hervorragende Analyseinstrumente und Verkäufer können dann abwägen, ob sie lieber noch 2-3 Jahre zur Entwicklung des Unternehmenswertes investieren möchten.

Wird ein Unternehmensverkauf geplant, kann durch die gezielte Prüfung des Geschäftsmodells und der bilanziellen Gestaltung der Unternehmenswert möglicherweise deutlich gesteigert werden. Alternativ kann über eine SWOT analysis angesetzt werden. Denn wird das Unternehmen gegen Risiken abgesichert, zum Beispiel mit speziellen Versicherungen, kann der Unternehmenswert gesteigert werden. Allerdings sind die Kosten dafür zur berücksichtigen.

Information Memorandum / Firmen-Exposé

The Information Memorandum, also Company Exposé genannt, hilft den Interessenten, einen umfangreichen Überblick über das Unternehmen zu erlangen. Neben einer kurzen Einführung zu der Geschichte, den Produkten und der strategischen Ausrichtung werden „harte“ und „weiche“ Faktoren aufgeführt. Die „harten“ Faktoren sind die Unternehmenszahlen, mit denen der Interessent einen Unternehmenswert ermitteln kann.

Zu den „weichen“ Faktoren gehören jene Punkte, die sich nicht oder nur teilweise quantifizieren lassen können. Hier werden zum Beispiel Führungsebenen, Market environment, staff training, unique selling propositions and customer and supplier relationships beschrieben. Die SWOT-Analyse ist hierbei ein mögliches Werkzeug zur Erstellung dieser Informationen.

Käuferansprache und Vermarktungsphase

Innerhalb der 4 Phasen des Verkaufsprozesses sollte die Käuferansprache unter keinen Umständen vernachlässigt werden.

Potenzielle Käufer / Unternehmensnachfolger

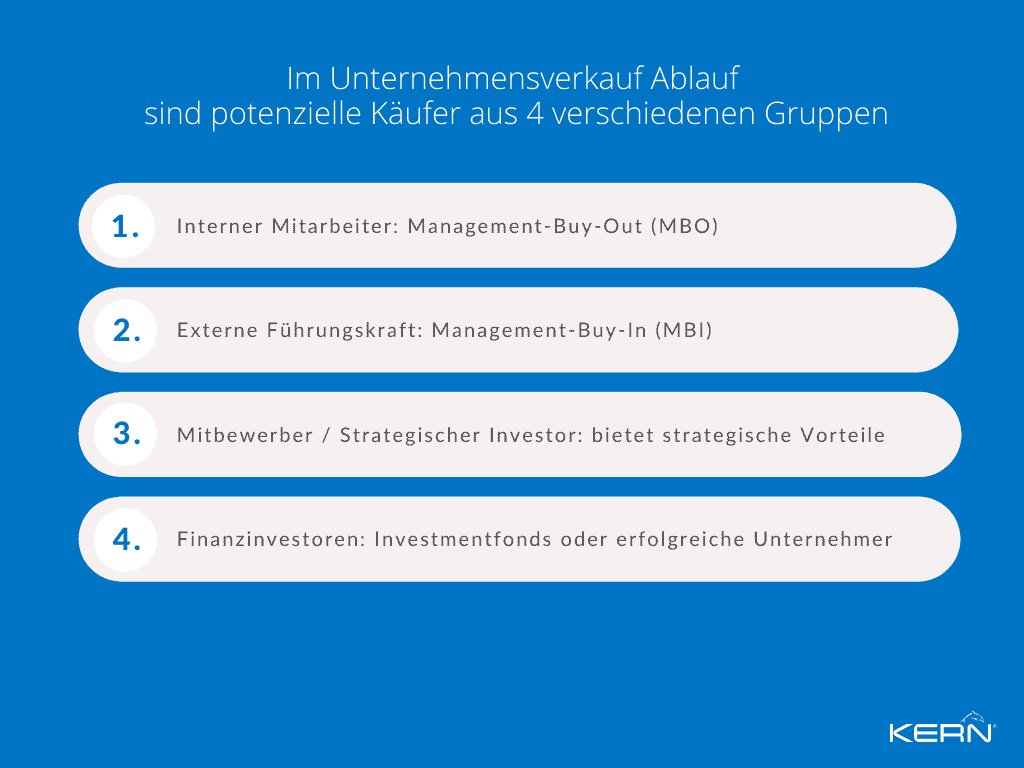

Ein Unternehmen kann an verschiedene Arten von Interessenten verkauft werden. Jeder Käufertyp sollte anders angesprochen werden, da verschiedene Investoren auch unterschiedliche Anreize an einer Unternehmenstransaktion haben.

Internal employee

At Management Buy Out (MBO) erwirbt das Management eines Unternehmens die Unternehmensanteile und erlangt so die Kontrolle über das Unternehmen. MBO’s sind häufig ein geplanter Generationenwechsel, bei dem der Käufer bereits im Vorfeld alle Informationen über das Unternehmen besitzt.

Externe Führungskraft

At Management Buy In (MBI) erwirbt ein unternehmensexterner Akteur die Kontrolle über das Unternehmen. Diese verfügen allerdings über deutlich weniger Informationen über das Unternehmen. Daher gestalten sich Kaufpreisverhandlungen häufig deutlich schwieriger als beim MBO.

Competitor / Strategic Investor

Die Übernahme eines Konkurrenten bietet eine Vielzahl strategischer Vorteile. So werden Customer and supplier relations, research and development results eingekauft und die Konkurrenz gleichzeitig verringert. Zudem können durch die Integration des übernommenen Unternehmens, in die Wertschöpfungskette des strategischen Investors, Synergien geschaffen werden und der eigene Unternehmenswert wird gesteigert.

Financial investors

Das Geschäftsmodell Buy company besteht für Finanzinvestoren darin, das gekaufte Unternehmen zu einem späteren Zeitpunkt mit Gewinn weiterzuverkaufen. Ziele von Finanzinvestoren sind häufig Start-ups or companies in growth sectors.

Finanzinvestoren sind oftmals Investmentfonds oder erfolgreiche Unternehmer, die bereits über eine große Menge an Kapital verfügen. Dieses wird in viele Unternehmen investiert, in der Hoffnung, dass die Investitionen in erfolgreiche Unternehmen überwiegen und zukünftig eine große Rendite erwirtschaften.

Aktive Käufersuche mit der Long List / Short List-Methode

The Long List/Short List method is a systematic procedure for the Identifikation und Klassifizierung potenzieller Käufer für das Unternehmen.

Auf der Long List werden alle Kriterien aufgelistet, die ein Käufer erfüllen sollte. Anhand dieser Liste werden alle passenden Käufer grob identifiziert.

Auf der Short List werden die Kriterien der Long List gewichtet. Es ergibt sich nun ein Ranking der am besten passenden potenziellen Erwerber. Diese können dann nach den wichtigsten Entscheidungskriterien weiter unterteilt werden.

Approach prospective buyers

Anhand der erstellten Klassen lassen sich die potenziellen Käufer gezielt ansprechen. Hierbei sollte der höchste Aufwand in die Umwerbung der Kandidaten der relevantesten Klasse fließen.

Sollte sich in der wichtigsten Klasse kein Kaufinteressent herauskristallisieren, werden Gespräche mit den Unternehmen der zweiten und eventuell der dritten Klasse intensiviert. Da sich diese Akteure vermutlich darüber bewusst sind, dass es besser passende Kauf-Kandidaten gibt, sollte für jede Zielgruppe eine individuelle Kommunikationsstrategie ausgearbeitet werden.

Passive Käufersuche mit einer Firmenbörse

Während mit der Long List/Short List-Methode aktiv nach potenziellen Erwerbern gesucht wird, ermöglicht es eine Firmenbörse, Investoren breit angelegt auf ein zu verkaufendes Unternehmen aufmerksam zu machen, die an einem Company acquisition interessiert sind. Hiefür erstellt der Unternehmer oder Berater ein anonymes Verkaufsinserat. Das Inserat sollte grundlegenden Informationen erwähnen und Neugierde auslösen.

Investoren können bei Interesse mit dem Verkäufer oder Berater dann in Kontakt treten und ein Kennenlernen kann erfolgen. Jeder Verkäufer, der dies selbst und direkt machen möchte, sollt sich vorab grundlegend über seine Anonymität Gedanken machen und überlegen, wie lange er diese aufrecht erhalten kann. Ein eingeschalteter Berater ist dem gegenüber der perfekte Sicherheitspuffer für eine lange Anonymität.

Mit einer Unternehmensbörse erhalten Sie qualifizierte Inserate von Interessenten

The confidentiality agreement

Ein Unternehmensverkauf ohne einen Austausch von Informationen zwischen Käufer und Verkäufer ist unmöglich. Das Non-Disclosure Agreement (NDA) soll verhindern, dass der Kaufinteressent die erhaltenen Informationen weitergibt oder veröffentlicht.

Zwar veröffentlichen Unternehmen jedes Jahr einen Jahresabschluss, in diesem sind jedoch viele sensible Informationen nicht enthalten. Und grundsätzlich stellt eine offene Verkaufsabsicht für einen Verkäufer ein potentielles Risiko dar.

Gelangen zum Beispiel die Verträge mit Zuliefern in die Hände eines Konkurrenten, könnte dieser sie nutzen, um die genauen Herstellungskosten des produzierten Produkts zu ermitteln und einen Preiskrieg beginnen. Daher sollten sensible Daten erst nach vereinbarter Geheimhaltung und verbindlicher Klärung eines nachhaltigen Investitionsinteresses weitergegeben werden.

Unternehmensprüfung und Verhandlung

Kein Unternehmenskauf kann ohne gründliche Prüfungen abgeschlossen werden. Sie bilden wichtige Säulen im Ablauf eines Kaufprozesses und für die Bestimmung des finalen Kaufpreises der Firma.

The due diligence

At the Due Diligence handelt es sich um eine Sorgfaltsprüfung, die mit einer Fülle von Fragen des Interessenten gezielt vorbereitet werden sollte. Ziel ist es, die Economic, tax and legal risks of a company acquisition to identify.

Hierzu bekommt der Interessent Einsicht in eine Fülle von Unternehmensdaten, dem sogenannten Datenraum. Mit fortschreitenden Verhandlungen und vertiefenden Fragen des Käufers kann dieser Datenraum erweitert werden.

Eine Due Diligence wird mehrheitlich vom Verkäufer erstellt und orientiert sich am Fragenbedürfnis des potentiellen Käufes. Eine Ausnahme kann bei größeren Firmen eine Vendor Due Diligence be.

Werden über die DD Risiken und Probleme bereits vor Eintritt in die finale Vertragsverhandlung mit einem Kaufinteressenten erkannt, können diese dem Interessenten in der Verhandlung mitgeteilt oder bis dahin behoben werden. Eine ausführliche und grundlegende Due Diligence schützt letztendlich beide Seiten vor möglichen Anspruchsrisiken nach einem Kauf.

The sale of a company from a tax perspective

Beim Unternehmensverkauf sind Steuern ein wichtiges Thema. Denn zum einen können bei der Übergabe der Kontrolle über ein Unternehmen Steuern anfallen, zum anderen versuchen Verkäufer bereits während der Due Diligence herauszufinden, wie zukünftige Steuern vermieden werden können.

If a business is passed down within the family, a Gift tax für den neuen Unternehmer anfallen, wenn das Unternehmen zu einem Preis unterhalb des Unternehmenswerts weitergegeben wird. Der Kaufinteressent prüft hingegen, welche Rechtsform für ihn Steuern einsparen kann. Bestimmte Rechtsformen und vertragliche Konstellationen können beiden Seiten helfen Steuern zu sparen.

The Due Diligence Checklist

Bei einer Due Diligence werden Unterlagen aus den Bereichen Jahresabschlüsse, Steuern, Finanzierung, Wettbewerbsanalyse, Vertrieb, Marketing, Einkauf und Logistik, Unternehmensorganisation, HR, Grundstücke und Gebäude sowie dem Gesellschaftsrecht verwendet.

Grundsätzlich sollten die Unterlagen die letzten 3-5 Jahre vollständig abbilden. Während Jahresabschlüsse und Marktanalysen für die Unternehmensbewertung verwendet werden, müssen alle Verträge (Gesellschaftervertrag, Kunden- und Lieferantenverträge, Arbeitsverträge) auf rechtliche Risiken überprüft become.

Die vollständige Übermittlung aller wichtigen Unterlagen ist besonders für den Verkäufer wichtig. Für alle Risiken, die dem Käufer bekannt waren, wird die Haftung übertragen. Werden Informationen zurückgehalten, muss der Verkäufer auch nach dem Unternehmensverkauf haften.

Take a look at our Due Diligence Checklist an, um mehr darüber zu erfahren, was im Einzelnen geprüft wird.

Contract and conclusion

Den letzten Schritt beim Ablauf eines Unternehmensverkaufs stellen die Vertragsmodalitäten dar. Der Verkaufsprozess nähert sich zwar dem Ende, die Aufmerksamkeit sollte aber weiterhin gewahrt werden. Häufig ist in diesem Stadium auf beiden Seiten eine starke emotionale Anspannung vorhanden. Die passende Kommunikation erhält damit einen besonders hohen Stellenwert für die Erreichung der finalen Unterschrift.

Asset Deal or Share Deal?

Die Übertragung einer Firma kann auf zwei verschiedene Weisen stattfinden. Beim Asset Deal verkauft das Unternehmen einzelne Wirtschaftsgüter an den Käufer. Dabei sollten alle Wirtschaftsgüter einzeln erfasst und übertragen werden.

Dies stellt sich in der Praxis oft als schwierig dar, besonders wenn immaterielle Vermögensgegenstände übertragen werden sollen, da der gesamte Kaufpreis auf die einzelnen Wirtschaftsgüter aufgeteilt werden muss. Neben Wirtschaftsgütern können auch Verbindlichkeiten übernommen werden.

At Share Deal hingegen werden nicht die Wirtschaftsgüter, sondern die Unternehmensanteile übertragen. Das bedeutet, die Kontrolle über das Unternehmen inklusive aller Aktiva und Passiva, wechselt vom Verkäufer zum Käufer.

Der Asset Deal bietet die Möglichkeit, nur bestimmte Teile eines Unternehmens zu übernehmen. So kann der Käufer das Haftungsrisiko minimieren, indem bestimmte Verbindlichkeiten nicht übernommen werden. Andererseits ist der Aufwand eines Asset Deals möglicherweise im Detail deutlich höher und Verträge mit Kunden oder Lieferanten könnten dabei einem Kündigungsrisiko unterliegen.

Read more about the topic in our technical article Share Deal vs. Asset Deal.

The bidding process

Das Bieterverfahren ist ein Prozess, bei dem aus dem Kreis der Interessenten der Höchstbietende ermittelt werden kann. Hierzu werden in einer ersten Phase alle Interessenten gebeten, ein unverbindliches Angebot zu erstellen. Anhand dieser Angebote sucht der Verkäufer die aussichtsreichsten Investoren aus.

Diese erhalten in einer zweiten Phase einen erweiterten Zugang zu internen Daten und können so ein verbindliches Angebot abgeben. In der letzten Phase erhalten diejenigen, die die besten Angebote abgegeben haben, Zugang zu den Most confidential information. Danach finden Vertragsverhandlungen mit diesen Interessenten statt. Dieses Verfahren ist klar strukturiert und in einem überschaubaren Zeitraum umsetzbar.

The Letter of Intent

The Letter of Intent (Absichtserklärung im Vorfeld einer anstehenden DD) ist ein wichtiges Hilfsmittel bei Vertragsverhandlungen. Beide Parteien halten ihre wichtigsten Absichten detailliert und schriftlich fest. So kann frühzeitig erkannt werden, ob eine Einigung überhaupt möglich ist.

The company purchase agreement

Konnten sich Käufer und Verkäufer bei der Vertragsverhandlung einigen, wird der Company purchase agreement erstellt. Dieser beschreibt alle verhandelten Punkte, wie die Anzahl der übernommenen Unternehmensanteile (beim Share Deal) und den Kaufpreis.

Zwar ist ein Unternehmenskaufvertrag für den Verkauf einer Firma grundsätzlich not bound to any particular form, allerdings können Vertragsbestandteile, wie zum Beispiel GmbH-Anteile oder Grundstücke, dazu führen, dass eine notarielle Beurkundung notwendig ist.

The Earn Out Clause

An important component of a company purchase agreement is the Earn Out Klausel. Diese sichert dem Verkäufer neben dem Kaufpreis einen erfolgsabhängigen Zusatzpreis zu. Hierbei legen Käufer und Verkäufer, Bedingungen und Betrag der späteren, weiteren Zahlungen, firm.

Eine solche erfolgsabhängige Zahlung dient in vielen Fällen als Kompromiss bei weit auseinanderliegenden Preisvorstellungen oder Risiken in der zukünftigen Entwicklung. Außerdem dient es als zusätzliche Motivation, falls der Unternehmer weiter für das Unternehmen arbeitet.

Abschluss der Transaktion – Signing und Closing

Der letzte Schritt des Unternehmensverkaufs ist die Unterschrift des Vertrags Signing sowie dessen Erfüllung Closing. Die Übertragung der Unternehmensanteile erfolgt, wenn alle erforderlichen Vertragsbedingungen, zum Beispiel Zahlung des Kaufpreises, erfüllt wurden.

Detailliertere Informationen und nützliche Tipps finden Sie zusätzlich in unserem Ratgeber zum Verkauf eines Unternehmens