Rund 70 % aller Unternehmer schätzen den Wert Ihres Unternehmens als zu hoch ein. Mit dieser Zahl eröffnete Ingo Claus von KERN – Unternehmensnachfolge – seinen Vortrag zum Thema Unternehmensbewertung in der IHK Osnabrück – Emsland – Grafschaft Bentheim.

Diese Überschätzung hat in der Praxis oft gravierende Folgen. Im Falle eines geplanten Unternehmensverkaufs führt eine zu hohe Bewertung nicht selten zu überhöhten Preiserwartungen und damit zu einer Unverkäuflichkeit des Unternehmens.

In Kürze: Wie berechnet sich der Unternehmenswert?

- The value of the entire company or a share in the company is determined by a company valuation.

- Material values, such as Fuhrpark, Maschinen und Grundstücke, as well as intangible assets, such as Employee expertise, brand, patents and experience of the staff are assessed.

- Unterschiedliche Bewertungsverfahren berücksichtigen dabei sowohl die Substanz des Unternehmens und wagen auf Basis vergangener Erträge eine Prognose für die Zukunft.

- Die Unternehmensbewertung ist für weitere Verhandlungen – etwa für eine Übergabe des Unternehmens – unabdingbar. Sie ist zwar not identical with the final purchase price, aber eine wichtige Basis für den Company sale.

- Es existieren verschiedene Methoden der Berechnung, die individuelle Vor- und Nachteile besitzen. Der über eine gut valide Unternehmensbewertung ermittelte Kaufpreiskorridor bietet einen Verhandlungsrahmen.

- The The capitalised earnings value method has gained acceptance in Germany.

Table of contents

Calculate enterprise value

Sie sind auf der Suche nach einer ersten Methode, um den Wert eines Unternehmens einzuschätzen? Unser Unternehmenswertrechner hilft Ihnen, den Wert eines Unternehmens basierend auf verschiedenen finanziellen Indikatoren und Kennzahlen schnell und einfach zu berechnen.

Um den Rechner zu verwenden, geben Sie einfach die erforderlichen Daten in die entsprechenden Felder ein und lassen Sie das Tool die Berechnungen für Sie durchführen.

Der Rechner bietet eine intuitive Benutzeroberfläche und berücksichtigt verschiedene Faktoren wie Gewinn und Branche, um Ihnen eine erste Einschätzung des Unternehmenswerts zu liefern.

Let us discuss the value of your business in a free initial consultation

What is the enterprise value

Der Unternehmenswert ist eine subjektive Bewertung aller materieller und immateriellen Vermögenswerte eines Unternehmens. Diese dient als Verhandlungsbasis bei Corporate transactionsbut can also be used as Key figure of a long-term corporate strategy serve.

Der Wert eines Unternehmens beschränkt sich allerdings nicht nur auf die Summe aller Vermögenswerte. Die Position of the company on the market, good reputation or synergies müssen ebenfalls bewertet werden. Dafür gibt es keine einheitliche Formel, sondern unterliegt vielmehr einer individuellen Betrachtung des Bewertenden.

If you use the Calculate enterprise value möchten, können Ihnen verschiedene Modellierungsverfahren bei der Schätzung des Unternehmenswerts helfen, jedoch ist nicht jedes Verfahren für jede Situation geeignet. Außerdem basieren alle Verfahren auf subjektiven Annahmen.

Daher können Käufer und Verkäufer arrive at different company values despite the same company figures.

Selbst bei dem Verkauf eines börsennotierten Unternehmens werden Verkaufspreise oberhalb der Marktkapitalisierung verhandelt, obwohl diese als beste Schätzung des Unternehmenswerts gilt.

Überhöhter Kaufpreis durch die s.g. Herzblut-Rendite

Während Unternehmer value not only the tangible assets but also the work and their heart and soul.they have invested in the company, an acquirer thinks first and foremost about what profits he can generate with the company in the future. Because of this different perspective, both sides often come to very different conclusions.

Für die Vergangenheit zahlt der Kaufmann nichts!

Mit der Erstellung einer Planungsrechnung für zumindest die kommenden drei Jahre tun sich viele Unternehmensinhaber schwer. Dieser Ausblick ist aber von großer Bedeutung, denn es gilt: Für die Vergangenheit zahlt der Kaufmann nichts!

Even if Enterprise value and purchase price not the same ist, besteht doch ein sehr enger Zusammenhang. Die glaubwürdige Herleitung des Ertragswerts dient damit nicht nur der Festsetzung der Kaufpreisforderung, sondern in den Verhandlungen auch der Enforcement of an attractive purchase price.

Es ist übrigens möglich, den Unternehmenswert zu steigern. Lesen Sie hierzu:

How to increase the value of your business and prepare for business succession

Methoden der Unternehmensbewertung in der Übersicht

Die Verfahren zur Unternehmensbewertung des Unternehmens lassen sich auf verschiedene Weise klassifizieren. Zum einen können Unternehmensbewertungen für die Fortführung oder die Auflösung einer Firma unterschieden werden. Für die Auflösung eines Unternehmens sollte der Liquidation value as a form of Substance value methods be used.

Des Weiteren kann eine unterschiedliche Datenbasis für die Bewertungen herangezogen werden. Die Substanzwertmethode verwendet hierzu Bilanzdaten, während Ertragswert- und Discounted cash flow methods Use data from the P&L.

Um als Verkäufer zu einer plausiblen und gleichzeitig well-founded purchase price claim für die anstehenden Gespräche mit potenziellen Käufern zu gelangen, ist eine professionelle Unternehmensbewertung erforderlich.

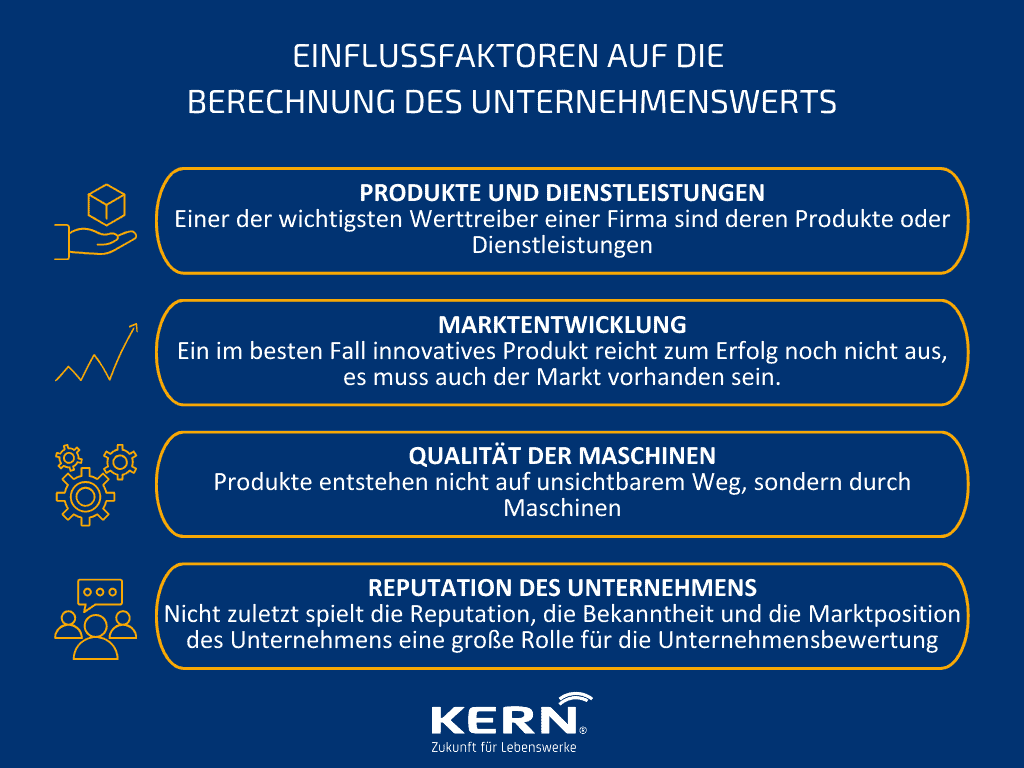

In den meisten Fällen haben Unternehmer keine oder falsche Vorstellungen, welcher Veräußerungserlös für ihr Unternehmen realistisch ist. Zudem gilt es, einen Überblick über die entscheidenden Faktoren bei den Bewertungsmethoden zu bewahren:

Looking ahead with the help of the capitalised earnings method

Neben dem Substanzwert- und Multiplikatorverfahren wird in Deutschland insbesondere das Ertragswertverfahren für die Bewertung von Unternehmen angewendet. Dies ist ein von Wirtschaft, Kammern und Finanzbehörden akzeptiertes Verfahren, das bei der Berechnung des Unternehmenswertes die Ergebnisse der Vergangenheit bereinigt, um anschließend eine möglichst plausible Zukunftsentwicklung zu prognostizieren.

Denn die Ergebnisse des Ertragswertverfahrens sind wesentlich abhängig von einer möglichst objektivierten Einschätzung der zukünftigen Überschüsse der Firma. In der Folge ist die realistische Risikoabschätzung für den zu ermittelnden Kapitalisierungszinsfuß besonders wichtig.

Finanzamt akzeptiert schlüssige Ertragswertbetrachtung

„Ein schlüssiges Wertgutachten nach dem Ertragswertverfahren akzeptiert das Finanzamt in der Regel und ist damit eine gute Alternative zum im § 199 des Bewertungsgesetz (BewG) definierten Verfahren“, unterstreicht Ingo Claus. Der Wert des Unternehmens orientiert sich damit eher am Marktwert. Denn die daraus resultierende geringere Steuerbelastung bzw. geringeren Abfindungssummen gegenüber Miterben führen somit zu einer geringeren finanziellen Belastung der zu übergebenden Unternehmen.

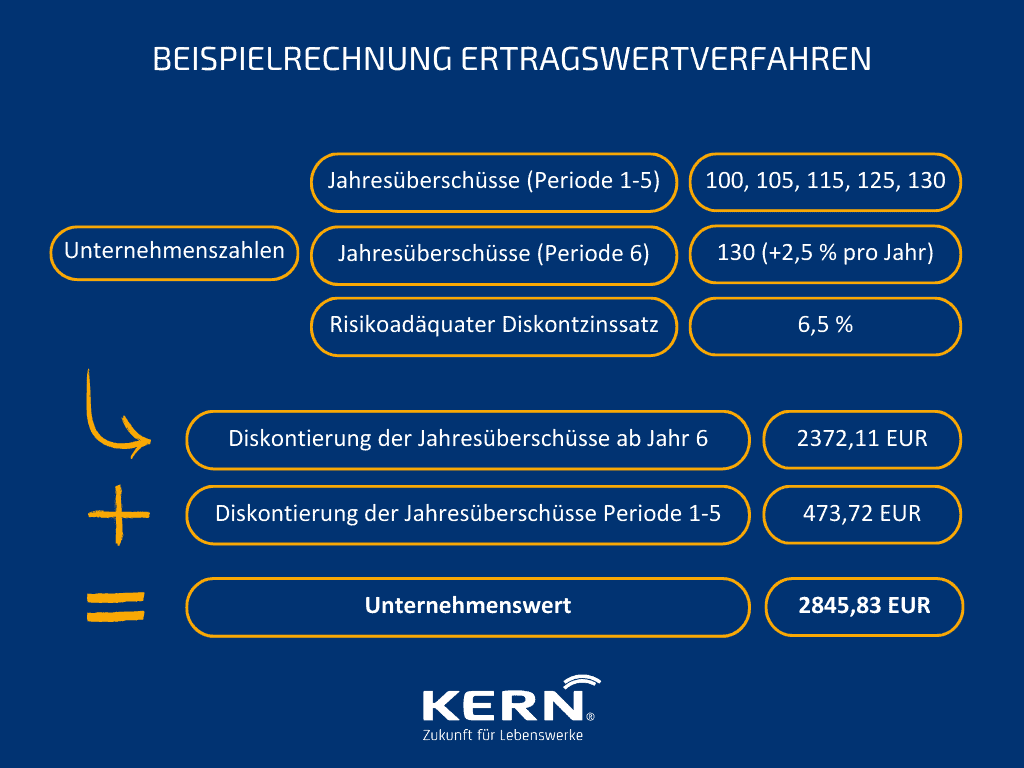

Example calculation of capitalised earnings value method

Advantages and disadvantages of the capitalised earnings method

Advantages:

In Deutschland weit verbreitetes und von den Finanzbehörden akzeptiertes Verfahren der Unternehmensbewertung

calculation compared to other methods slightly

Adaptable risk factor

Disadvantages:

Risikofaktor bietet Möglichkeit der Manipulation

Forecasting the future not always suitable

The net asset value method

Der Substanzwert kann für eine Unternehmensfortführung oder eine Unternehmensauflösung berechnet werden. Bei letzterer wird der Liquidationswert berechnet. Um den Liquidationswert zu berechnen, werden die Marktwerte aller bilanzierten und nicht bilanzierten Vermögenswerte addiert und alle ausstehenden Verbindlichkeiten abgezogen, denn diese müssen von dem Verkaufserlös bedient werden.

Zusätzlich müssen alle durch die Liquidation entstandenen Kosten abgezogen werden. Der The advantage of the net asset value method is a relatively simple calculation of the value einer Unternehmensauflösung. Zudem kann dieses Bewertungsverfahren als Untergrenze des Unternehmenswertes bei Unternehmensfortführung dienen.

Der eigentliche Substanzwert oder Fortführungsstatik basiert nicht auf der Annahme einer Zerschlagung des Unternehmens. Es handelt sich hierbei um folgende Opportunitätskostenbetrachtung: Der Wert des Unternehmens entspricht den Kosten, die bei der Erschaffung einer exakten Kopie des Unternehmens entstehen würden. Also wenn auf ein gleichwertiges Grundstück mit gleichwertigen Immobilien und mit gleichwertigen Maschinen gekauft werden würde.

This means that the net asset value is based on the Wiederbeschaffungsaltwert des bilanzierten Vermögens und des nicht bilanzierten Vermögens.

The restoration value must be distinguished from the liquidation value. The latter arises from the break-up of the enterprise and the subsequent Sale of the individual elements.

Der Liquidationswert entspricht dabei dem Betrag, der durch die Zerschlagung des Unternehmens sowie dem anschließenden Einzelverkauf erzielt werden kann.

Der Liquidationswert des nicht betriebsnotwendigen Vermögens kann zusätzlich angesetzt und the borrowed capital must be deducted. Das Substance value method hat weiterhin den Vorteil, dass von einem fortgeführten Unternehmen ausgegangen wird, dies ist bei den meisten Unternehmenstransaktionen der Fall.

However, one important factor is not considered: das „Know-how“ des alten Unternehmens. Denn Arbeitsabläufe und geschultes Personal mit Erfahrung an diesen Maschinen lassen sich weder kopieren noch bewerten.

Advantages and disadvantages of the net asset value method

Advantages:

Simple calculation

„Greifbarer Wert“, der auch für Laien geeignet ist

Disadvantages:

Vernachlässigung von Faktoren wie Kundenstamm oder Wettbewerbsposition

Keine Berücksichtigung der Profitabilität

Discounted cash flow method (DCF method)

Bei der Discounted Cash Flow Methode werden die freien (verfügbaren) Cashflows als Ausgangspunkt für die Unternehmensbewertung verwendet. Der Unternehmenswert entspricht dabei der Summe der mit einem risikoadäquaten Zinssatz abgezinsten freien Cashflows.

Für die Schätzung der freien Cashflows können die Geschäftspläne der folgenden Jahre individuell erstellt werden. Alternativ kann das Value generators Rappaport process can be applied. Here, starting from current Data such as turnover, return on sales and investment in working capital und einem geschätzten zukünftigen Umsatzwachstum die Freien Cashflows berechnet.

The DCF method can be applied in 2- or 3-phase models. In the first phase die Cashflows für die nächsten 5 bis 10 Jahre individuell geschätzt. In the last phase, a constant free cash flow or a cash flow with constant growth is assumed.

Die Zwischenphase im 3-Phasen-Modell soll einen Übergang zwischen der letzten geplanten Phase und der Restwertphase plausibel modellieren. Hierbei wird meistens von einer linearen oder exponentiellen Diffusion der Cashflows über 3 bis 5 Jahre gone out.

The Advantage of the discounted cash flow methods ist, dass es sich auf aktuelle Unternehmenszahlen stützt. Dadurch wird die Ausgangssituation bestmöglich modelliert. Allerdings hängt der Unternehmenswert stark von 2 Faktoren ab, dem risikoadäquaten Diskontzinssatz und der freien Cashflows in der ersten Phase. Eine falsche Schätzung dieser führt zu großen Abweichungen.

Advantages and disadvantages of the discounted cash flow method

Advantages:

Gute Anpassungsfähigkeit auf individuelle und aktuelle Unternehmenssituationen

Result well comparable

Macht eventuelle Risiken der Investition frühzeitig deutlich

Disadvantages:

Risk factor can be a weak point in case of poor choice

Forecasting the future not always suitable

Multiplier procedure

Die Multiplikatormethode ist eine grobe Schätzung des Unternehmenswerts. Hierbei werden der Börsenwert und in der Vergangenheit getätigte Unternehmenstransaktionen analysiert und mit Bilanzkennzahlen in Verbindung gesetzt. So haben sich gängige Multiplikatoren entwickelt. Für eine genaue Bestimmung des richtigen Multiplikators, werden nur die Unternehmenstransaktionen von vergleichbaren Unternehmen verwendet.

Diese Verfahren eignen sich besonders für eine Plausibilitätsprüfung des mit anderen Verfahren berechneten Unternehmenswerts. Gleichwohl bilden die öffentlich zugänglichen Multiplikatoren immer nur Bewertungskorridore vergangener Transaktionen ab. Da ein Unternehmen nicht beliebig vergleichbar ist, müssen entsprechende Bereinigungen und Plausibilisierungen im Vorfeld einer Multiplikatorbewertung vorgenommen werden. Dies gilt es zu berücksichtigen.

Advantages and disadvantages of the multiplier method

Advantages:

Widely used assessment methodology

Can be calculated quickly and easily

Benötigt wenige Daten für erste Ergebnisse

Disadvantages:

Due to the lack of data, not very accurate

Multiplikator ist eine Schwachstelle, über die gestritten werden kann

Eine Anwendung ohne entsprechende Analyse, nachfolgende Bereinigung und Plausibilisierung führt oftmals zu deutlich überhöhten Unternehmenswerten.

The venture capital method

Mit der Venture-Capital-Methode können Start-ups bewertet werden. Der Value of these companies lies in the development of new concepts and technologies, nicht in Vermögenswerten, Umsätzen oder positive Cashflows. Daher können die vorangegangenen Bewertungsverfahren nicht angewendet werden.

Therefore, the value of the company is first calculated at a time when it is comparable to other companies, for example in 10 years. Dieser Unternehmenswert wird dann über die angenommene Dauer diskontiert. Allerdings wird ein höherer Diskontzinssatz verwendet als bei etablierten Unternehmen, denn das Risiko ist wesentlich höher.

Da eine zahlenfreie Bewertung oftmals nicht zielführend sein kann, wird im deutschsprachigen Raum oftmals auf die Venture-Capital-Methode verzichtet und stattdessen die oben beschriebene DCF-Methodik eingesetzt.

Advantages and disadvantages of the venture capital method

Advantages:

Ermöglicht eine Berechnung trotz fehlender Daten

Disadvantages:

Uncertain and complex

Unternehmensbewertung nach den Grundsätzen des IDW

Branchenübliche Multiplikatoren reichen zur Ermittlung eines Unternehmenswertes oft nicht aus, da sie nicht auf den Einzelfall zugeschnitten und oft veraltet sind. Zur Ermittlung einer Unternehmensbewertung nach den Grundsätzen des Instituts der Wirtschaftsprüfer in Deutschland (IDW) analysieren wir die Jahresabschlüsse der vergangenen drei Geschäftsjahre und erstellen mithilfe der Unternehmensplanung einen Ertragswert.

Der Ertragswert ist identisch mit den auf den Bewertungsstichtag abgezinsten, zukünftig zu erzielenden ausschüttungsfähigen Erträgen. Die Abzinsung erfolgt dabei mittels eines an das jeweilige unternehmerische Risiko angepassten Zinssatz.

Die Grundsätze des IDW sind das IDW-S1 = Ertragswertverfahren. Dabei handelt es sich um die vom Finanzamt akzeptierte Methode der Unternehmensbewertung und schließt die typischen Fehler einer Multiplikatorbewertung durch eine fundierte IDW-S1 aus.

FREE expert guide: How to make your business succession a success.

Valuation SME

Laut dem Institut für Mittelstandsforschung (IfM) werden jedes Jahr in Deutschland mehr als 20.000 KMU Unternehmen mit einer ungelösten Company succession confronted. If you too want to change your Sell company the first step towards a regulated succession should be a well-founded evaluation of the company.

Da die Methodiken zur Wertermittlung analog bei großen und kleinen Unternehmen Anwendung finden, stellt sich die Frage, ob es nicht doch ein paar Small but crucial differences in the valuation of SMEs gives.

Qualitative characteristics

Die Abgrenzung zu großen Unternehmen erfolgt nicht nur anhand von Kennzahlen und Finanzparametern. Das heißt, dass SMEs have a few very specific characteristicsthat work well in Ihlau, Duscha, Gödecke: Besonderheiten bei der Bewertung von KMU (Seite 6 ff.) beschrieben werden. Danach sind die Merkmale in die 4 Bereiche Geschäftsmodell, Eigner, Informationen und Finanzierung zu unterteilen.

Beispielsweise ist ein elementarer Unterschied zu großen Unternehmen der beschränkte Zugang zum Kapitalmarkt und die oftmals niedrige Eigenkapitalquote. Hinzu kommen der starke Einfluss der Eigentümer und die fehlende Diversifikation. Vereinfachte Prozesse im Rechnungswesen oder eine fehlende Unternehmensplanung beziehungsweise ein vereinfachtes Controlling bringen die entscheidenden Unterschiede ans Licht.

Vor diesen Hintergründen stellt sich natürlich umso mehr die Frage, ob die Business valuation of SMEs not fundamentally different must/should be.

Business valuation of SMEs

In Moxter 1983, p. 123 fällt der Satz: „Bewerten heißt vergleichen“. Das ist das Grundprinzip einer jeden Unternehmensbewertung. Das bedeutet beispielsweise, dass beobachtbare Preise oder Renditen für ähnliche Vermögenswerte verglichen werden. Genau in diesem Punkt unterscheidet sich aber eine Bewertung von großen Unternehmen. Nicht in der Methodik, aber in der Komplexität.

Natürlich ist eine Konzernbewertung höchst komplex und alles andere als trivial. Aufgrund des Mangels an Vergleichswerten ist the valuation of an SME is no less complex. Gerade die KMU sind aufgrund der oft sehr speziellen und spezifischen Merkmale nur sehr beschränkt mit herangezogenen Vergleichsunternehmen vergleichbar.

In Deutschland hat sich für KMU das Ertragswertverfahren durchgesetzt. Dies basiert auf den gegebenen Bewertungsanlass in diesem Umfeld. Anders als im Transaktionsumfeld, wo das DCF-Bruttoverfahren meist angewendet wird, haben ist der Bewertungsanlass für ein KMU oftmals als Bewertungsanlass eine anstehende Unternehmensnachfolge.

In diesem Rahmen muss selbstverständlich auch eine sound analysis erfolgen und die speziellen Gegebenheiten des KMU berücksichtigt werden. Im Vordergrund dabei steht die Ermittlung der zukünftig erzielbaren Umsätze (unter Berücksichtigung der neuen oder alten Inhaber) und ein passender, risikoäquivalenter Kapitalisierungszinssatz.

Der Preis für das Unternehmen ist letztendlich das Ergebnis von Angebot und Nachfrage und natürlich einer gut geführten Verhandlung.

Typical mistakes in business valuation

Avoid the 7 most expensive mistakes in business valuation! In a exclusive online seminar our experienced expert gives you the best tips on how the value and price of a venture should be composed.

Bei der Unternehmensbewertung können schnell Fehler entstehen. Die typischen Fehler lassen sich auf drei Fehlerquellen zurückführen.

The use of inconsistent data:

- Use of inconsistent data (e.g. mixing real and nominal values)

- Verwendung von indirekten/errechneten Daten führt zu falschen Abhängigkeiten (z. B. Abschreibungen, Zinsen und Dividenden hängen nicht direkt vom Umsatz ab)

Bei der Abzinsung werden oft folgende Faktoren vernachlässigt:

- Unterschiedliche risikolose Zinssätze für längere und kürzere Perioden

- Distinction between secure and uncertain cash flows and their correct discount rate

Modelling error:

- Bewertungsmodell passt nicht zur zukünftigen Unternehmensstrategie

- Valuation model does not fit comparable companies

- Unternehmensbewertung wird nur für ein Szenario erstellt, Sensitivitätsanalyse und Monte-Carlo-Simulation werden nicht verwendet

Conclusion

Wenn Sie eine passende Unternehmensbewertung, etwa für den Company acquisition, vornehmen möchten, sollten sie vorher unbedingt die Ziele der Bewertung bestimmen und eine für den Bewertungszweck geeignete Methoden wählen. Wie Sie gelernt haben, bestehen große Unterschiede in der Bewertung von KMUs, Großunternehmen oder Start-ups.

Für Familienunternehmen ist in vielen Fällen die Ermittlung der Unternehmensbewertung auf Basis des Ertragswertverfahrens meaningful. We are happy to help you with our advice on this important topic.