Das Thema Nachfolgeplanung ist ein wichtiger Schritt, um die Kontinuität und den zukünftigen Erfolg eines jeden Unternehmens zu gewährleisten. In diesem Artikel geben wir Ihnen einen umfassenden Überblick über alle wichtigen Informationen zur Sicherung einer erfolgreichen Nachfolgelösung für Ihr Unternehmen.

Read briefly

- Entrepreneurs should take into account the Nachfolge für ihr Lebenswerk bereits frühzeitig planen

- Der Unternehmensnachfolger kann aus der eigenen Familie stammen, aus dem Betrieb oder ein externer Käufer sein

- Für eine erfolgreiche Umsetzung sind gründliche Vorbereitung sowie Aufbereitung der Dokumente für den Firmenübertrag crucial

- Finden Sie Interessenten für den Unternehmenskauf auf unserer Unternehmensbörse

Table of contents

Definition of business succession

Unternehmensnachfolge ist der Prozess der Übertragung des Eigentums an einem Unternehmen von einer Person oder einer Gruppe von Personen auf eine andere. Die Nachfolgeplanung ist ein wichtiger Bestandteil der Unternehmensnachfolge, da sie sicherstellt, dass ein Unternehmen auch dann noch erfolgreich und profitabel ist, wenn der oder die derzeitigen Eigentümer in den Ruhestand gehen oder das Unternehmen verlassen.

Forms of business succession

Eine klare Übersicht der verschiedenen Formen der Unternehmensnachfolge hilft dabei, die richtige Lösung für Ihr Unternehmen zu finden. Zu den häufigsten Optionen gehören:

- Passing on the business to family members – dies wird oft als „familieninterne Nachfolge“ bezeichnet

- Sale of the company to an external party – dies kann eine Privatperson oder ein Unternehmen sein

- Merger with another company or entering into a joint venture

- Ein Management Buy Out (MBO) – hierbei übernehmen die derzeitigen Manager das Eigentum und die Kontrolle über das Unternehmen

- Sale of parts of the company – dies könnte den Verkauf von Geschäftsbereichen, Produktlinien oder anderen Vermögenswerten beinhalten

In the family or rather externally?

At Medium-sized companies stellt sich häufig die Frage, ob die Unternehmensnachfolge innerhalb der Familie oder durch einen externen Nachfolger geregelt werden soll. Beide Optionen bieten spezifische Vor- und Nachteile.

For example, if the family business is complex and several family members are involved, a externer Fachmann oder ein strategischer Investor neue Impulse setzen und das Unternehmen dadurch auf eine neue Entwicklungsstufe führen.

Wenn andererseits ein Familienmitglied das Unternehmen und seine Abläufe sehr gut kennt, für das Unternehmen brennt und gut ausgebildet ist, ist es vielleicht besser geeignet, die Nachfolge anzutreten.

Letztlich gibt es verschiedene Optionen, die detailliert betrachtet und bewertet werden müssen, um am Ende die passende Lösung für den Betrieb zu finden.

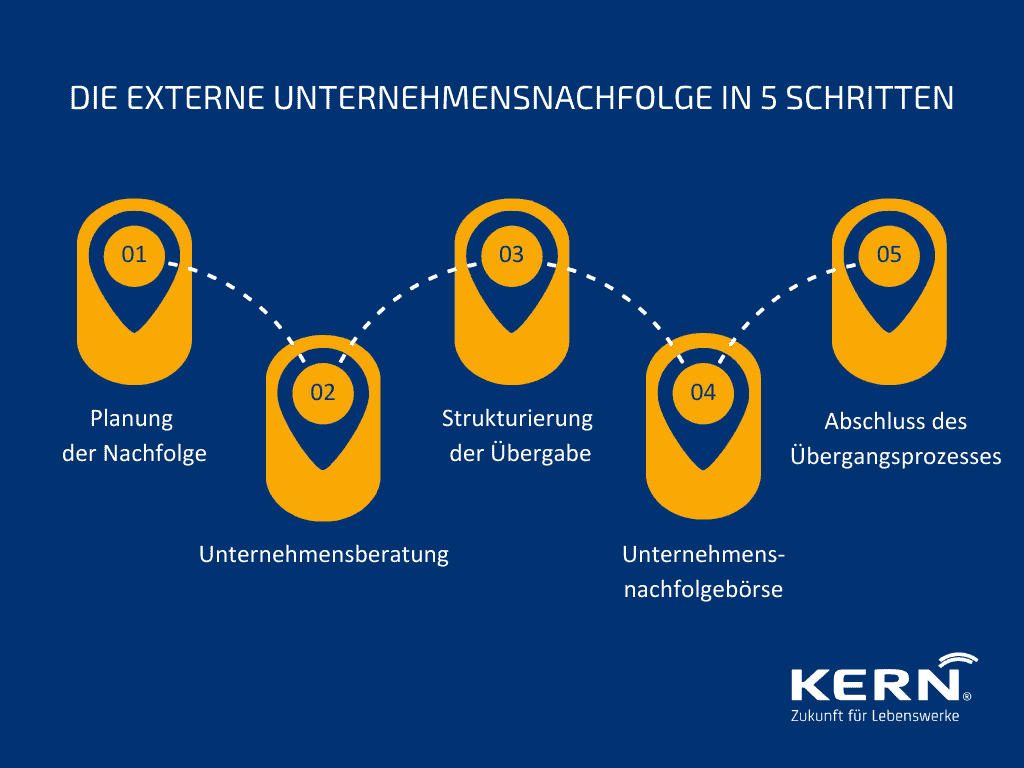

External company succession in 5 steps

Die Planung für die Zukunft Ihres Unternehmens ist entscheidend. Mit den richtigen Strategien können Sie eine erfolgreiche Übernahme vorbereiten und einen reibungslosen Übergang sicherstellen.

Step 1: Succession planning

Succession planning is about the preparation of a geordneten Übergangs von Führungspositionen, Verantwortlichkeiten und Eigentumsverhältnissen in einem Unternehmen. Zur Planung gehört auch die gesamte Organisation einer Firma übergabefähig zu gestalten. Dieser Prozess umfasst im ersten Schritt unbedingt einen Zeitplan, der allen Beteiligten als Orientierung dient.

Step 2: Business valuation

Ein wichtiger Schritt bei der Vorbereitung des Verkaufs ist die Ermittlung des Unternehmenswerts, um eine Orientierung zu haben, welchen Verkaufspreis der Verkäufer erwarten kann. Gängige Verfahren sind hierfür eine Einschätzung über das Multiple-Verfahren oder eine objektivierte Berechnung über das Income approach according to IDW S1.

Schritt 3: Strukturierung der Übergabe

Die Strukturierung der Unternehmensübergabe umfasst die Aufbereitung und Erstellung notwendiger Dokumente und Berichte, etwa des Firmenexposés oder der Finanzberichte. Unklarheiten und eventuelle Stolpersteine sollten bekannt sein. Sie wollen einem möglichen Käufer keine unvollständigen Dokumente präsentieren oder Dokumente erst nach Anfrage erstellen müssen.

Je gründlicher die Vorbereitungen in dieser Phase absolviert werden, desto reibungsloser kann der Verkaufsprozess vonstattengehen.

Schritt 4: Unternehmensnachfolgebörse

A Nachfolgebörse bietet Unternehmen die Möglichkeit, sich gezielt auf dem Market zu positionieren und potenzielle Käufer oder Nachfolger zu finden. Sie ermöglicht Interessenten den Zugriff auf Informationen über potenzielle Nachfolger und ermöglicht es Verkäufern, ihre Unternehmen zum Verkauf anzubieten.

Die Anonymität kann über M&A-Berater gewährleistet werden oder direkte Inserate sollten so neutral sein, dass eine Identifizierung im ersten Austausch nicht möglich ist.

Die Börse bietet einen Online-Marktplatz, auf dem Käufer und Verkäufer wichtige Details einer möglichen Transaktion erfahren können. Darüber hinaus bieten einige Anbieter unterstützende Dienstleistungen wie Due-Diligence-Prüfungen (Due Diligence = Sorgfaltsprüfung) und Finanzanalysen an, um sicherzustellen, dass die Transaktion auf faire und transparente Weise durchgeführt wird.

Schritt 5: Abschluss des Übergangsprozesses

Die vierte Phase der Unternehmensnachfolge ist der Abschluss des Übergangsprozesses. In dieser Phase muss sichergestellt werden, dass alle rechtlichen, finanziellen und betrieblichen Anforderungen erfolgreich erfüllt wurden, um einen reibungslosen Übergang von der derzeitigen Führung auf die neue Führung zu gewährleisten.

In dieser Phase müssen alle Dokumente für den Übertrag auf einen neuen Eigentümer ordnungsgemäß aktualisiert und bei den zuständigen Behörden, wie den Steuerbehörden oder Aufsichtsbehörden, eingereicht werden. Weiterhin sollten alle anderen notwendigen Schritte unternommen werden, um einen erfolgreichen Übergang zu gewährleisten. Eine Option ist hierbei die Erstellung eines Firmenhandbuchs, in dem die alten und ggf. neuen Richtlinien, Kompetenzen, Verantwortlichkeiten und Verfahren beschrieben werden.

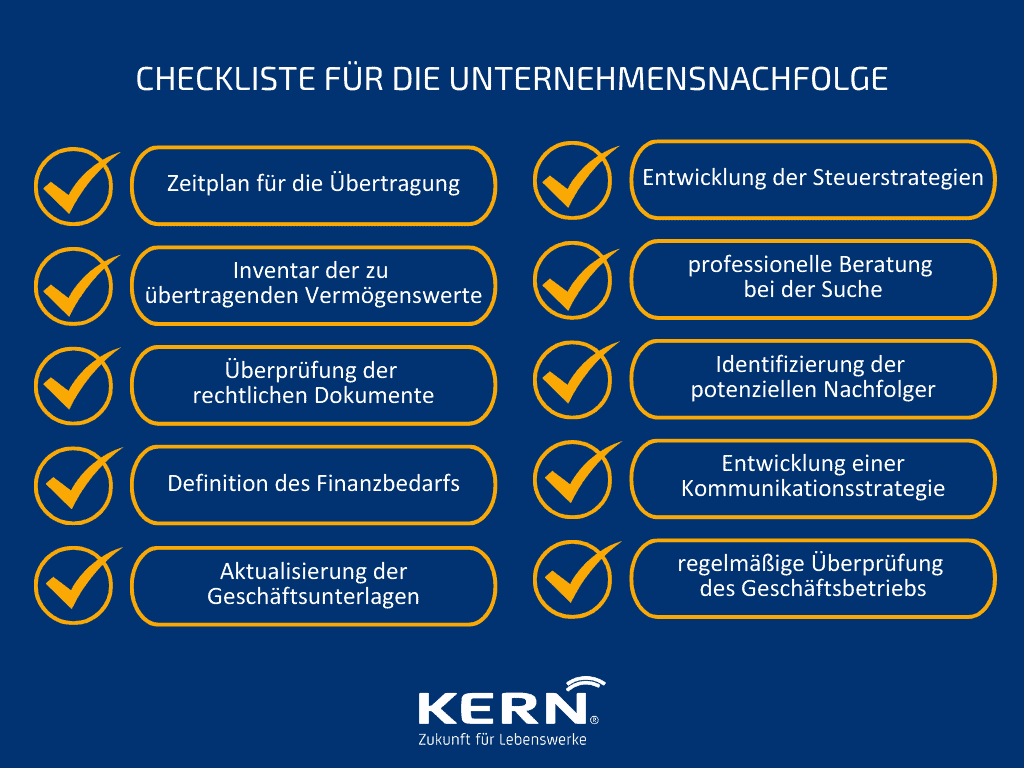

Checkliste für Ihre Unternehmensnachfolge

- Place a Zeitplan für die Übertragung von Vermögenswerten, Führungspositionen und Verantwortlichkeiten firm.

- Erstellen Sie ein Inventar der zu übertragenden Vermögenswerte und Verbindlichkeiten des Unternehmens.

- Überprüfen Sie die vorhandenen rechtlichen Dokumente, einschließlich der Geschäftsverträge und Versicherungspolicen.

- Determine the financial needs related to succession planning.

- Aktualisieren Sie die Geschäftsunterlagen, um die Änderungen bei den Eigentumsverhältnissen und den Managementaufgaben zu berücksichtigen.

- Develop control strategies to reduce the Tax burden to be reduced to a minimum through skilful action.

- Use Professional advice during the search nach geeigneten Nachfolgern. Neben einem ausgezeichneten Netzwerk liegt der größte Vorteil eines qualifizierten Beraters in seiner emotionalen Neutralität. Nur ein Fachmann kann die Anliegen aller Beteiligten abwägen und zusammenführen.

- Identify potential successors and assess their qualifications.

- Develop a communication strategy to inform employees, customers, suppliers and other stakeholders after the sale.

- Überprüfen Sie den Geschäftsbetrieb regelmäßig und nehmen Sie bei Bedarf Anpassungen vor, um einen reibungslosen Nachfolgeprozess zu gewährleisten.

3 Tipps für die erfolgreiche Unternehmensnachfolge

Seit 2004 unterstützen wir unsere Mandanten beim Generationswechsel oder dem Verkauf ihres Lebenswerkes. Aus unserem großen Erfahrungsschatz möchten wir Ihnen an dieser Stelle drei Tipps mitgeben.

No. 1 Implementing company succession tax-free

A Company succession tax-free zu gestalten ist möglich, wenn ein Unternehmen von einer Generation innerhalb der Familie vererbt wird, der Nachfolger den Betrieb aber auch aktiv weiterführt. Durch ein sogenanntes 5-Jahres bzw. 7-Jahres-Modell kann die Tax burden reduced by 85 % or even 100 % become.

Da es gewisse Fallstricke gibt, die beachtet werden sollten, und es zudem Sinn macht, die Nachfolge sehr frühzeitig zu planen, beraten wir Sie gerne. Grundsätzlich ist immer der Einzelfall zu betrachten.

Erweitert gibt es auch steuerliche Optimierungen, wenn vor einem Verkauf frühzeitig Übertragskonstrukte vorbereitet werden.

Nr. 2 Der optimale Zeitpunkt für die Unternehmensnachfolge wählen

Der optimale Zeitpunkt für Unternehmensnachfolgen hängt von den spezifischen Bedürfnissen des Unternehmens und seiner Eigentümer ab. Im Allgemeinen wird empfohlen, dass die Nachfolgeplanung einige Jahre vor dem Ausscheiden des Eigentümers oder der wichtigsten Mitarbeiter beginnt.

So bleibt genügend Zeit, um einen Nachfolgeplan zu entwickeln, potenzielle Nachfolger zu finden, einzustellen und einen reibungslosen Übergang zu gewährleisten. Alternativ direkt das Unternehmen an Dritte zu verkaufen.

Nr. 3 Alle Finanzierungsmöglichkeiten zur Unternehmensnachfolge ausschöpfen

Funding for this process can come from a variety of sources, including Banken, Sparkassen, Risikokapitalgeber, Finanz-Investoren und staatliche Zuschüsse oder Bürgschaften. Unternehmer können sich nicht nur an externe Investoren wenden, sondern auch Familienmitglieder um Hilfe bitten, um das notwendige Kapital zu beschaffen.

Um einen erfolgreichen Übergang zu gewährleisten, ist es wichtig, im Voraus zu planen und alle verfügbaren Optionen zu kennen.

Häufige Fehler bei der Nachfolge für Unternehmen

Um sicherzustellen, dass der Übergang reibungslos verläuft, ist es wichtig, Fehler zu vermeiden. Hier sind einige häufige Fehler, die Unternehmer bei der Planung der Unternehmensnachfolge vermeiden sollten:

- Planning in advance

Viel zu oft warten Unternehmer, bis sie kurz vor dem gewünschten Ruhestand stehen oder von einer Krankheit dazu gezwungen werden, bevor sie an die Nachfolgeplanung denken. Dies kann zu Problemen führen, da möglicherweise nicht genug Zeit bleibt, um das Eigentum ordnungsgemäß zu übertragen und einen reibungslosen Übergang zu gewährleisten. Eine erfolgreiche Nachfolgeplanung erfordert die sorgfältige Berücksichtigung aller Aspekte des Übergangs, einschließlich rechtlicher Anforderungen, Steuern und Altersversorgung. Eine vorausschauende Planung kann dazu beitragen, dass diese Fragen rechtzeitig geklärt werden. Ein Verkauf unter Zeitdruck drückt auch den Preis. - No involvement of family members

Die Familienmitglieder sollten über alle Aspekte und Gründe der Nachfolgeplanung informiert und nach Möglichkeit in den Prozess einbezogen werden. Wenn Sie die Familienmitglieder nicht einbeziehen, kann dies zu Unstimmigkeiten und Verwirrung darüber führen, wer das Unternehmen übernimmt, wenn der derzeitige Eigentümer in den Ruhestand geht oder stirbt. Die frühzeitige Einbindung von Familienmitgliedern kann dazu beitragen, spätere Missverständnisse über die zukünftige Führungs- und Eigentumsstruktur zu vermeiden. - Do not seek professional advice

Unternehmenseigentümer sollten einen erfahrenen Berater konsultieren, bevor sie wichtige Entscheidungen im Zusammenhang mit ihrer Unternehmensnachfolge treffen. Diese Fachleute können wertvolle Ratschläge zum Schutz von Vermögenswerten, zum Steuermanagement, zur Eigentumsübertragung und zu anderen wichtigen Fragen im Zusammenhang mit der Nachfolgeplanung geben. - Do not formulate clear expectations

Wenn ein Unternehmen von einer Person auf eine andere übertragen wird, ist es von entscheidender Bedeutung, dass alle Beteiligten die Erwartungen hinsichtlich der Rollen und Verantwortlichkeiten in der neuen Organisationsstruktur nach dem Übergang klar definiert haben. Ohne klar definierte Erwartungen können Konflikte entstehen, die den gesamten Übergangsprozess stören oder verzögern können. - Ignoring potential risks

Unternehmer sollten auch die potenziellen Risiken in Betracht ziehen, die mit der Übertragung des Eigentums an ihrem Unternehmen verbunden sind – Risiken wie der Verlust der Kontrolle über die Entscheidungsprozesse oder potenzielle Streitigkeiten zwischen den Familienmitgliedern darüber, wem welcher Teil des Unternehmensvermögens nach Abschluss der Übergabe gehören wird. Durch die frühzeitige Identifizierung potenzieller Risiken im Zusammenhang mit ihrer speziellen Situation können sich Unternehmer besser auf mögliche Probleme vorbereiten, die nach dem Übergang auftreten könnten, und sich entsprechend dagegen schützen. Ähnliche Anliegen gilt es auch gegenüber fremden Dritten zu beachten.

Conclusion

Zusammenfassend lässt sich sagen, dass es wichtig ist, einen erfolgreichen und reibungslosen Übergang von einer Führungsgeneration zur nächsten in einem Unternehmen sorgfältig zu planen und umzusetzen.

Wenn Sie unseren empfohlenen fünf Schritten folgen, können Sie eine erfolgreiche Unternehmensnachfolge gewährleisten. Mit einer durchdachten Planung können Unternehmen sicherstellen, dass das Unternehmen auch für kommende Generationen gesund bleibt.

FAQ

Welche Risiken können bei einer Unternehmensnachfolge auftreten?

Es können verschiedene Risiken auftreten, wie beispielsweise die Anpassung des neuen Nachfolgers an die Unternehmenskultur, die finanzielle Belastung durch den Kaufpreis oder die erfolgreiche Weiterführung des Unternehmens.

Welche Chancen ergeben sich für Nachfolger?

Im Gegensatz zu Existenzgründungen bietet sich die Chance, ein bereits funktionierendes Unternehmen zu übernehmen und weiterzuentwickeln. Dabei kann man von bereits etablierten Kundenbeziehungen, einem bestehenden Produkt oder einer Dienstleistung sowie dem Know-how des Unternehmens profitieren.

Was sollte man beachten, wenn man als Führungskraft eine Übernahme in Betracht zieht?

Als Führungskraft ist es wichtig, die eigenen Fähigkeiten und Qualifikationen zu überprüfen, die Kommunikation mit dem aktuellen Eigentümer des Unternehmens zu suchen und die finanziellen Aspekte der Nachfolge zu klären.

What role does external succession play in a business succession?

Die externe Nachfolge kann eine attraktive Option sein, wenn innerhalb der Familie kein geeigneter Nachfolger gefunden werden kann. Hierbei wird ein externer Nachfolger gesucht, der das Unternehmen übernimmt und weiterführt.

What is particularly important in succession planning?

Unternehmerinnen und Unternehmer sowie Inhaberinnen und Inhaber sollten die Nachfolge frühzeitig planen, um rechtliche und organisatorische Hürden zu vermeiden. Dabei ist es entscheidend, klare Zuständigkeiten festzulegen und die Übergabe strukturiert vorzubereiten. Eine professionelle Beratung hilft, individuelle Ziele umzusetzen und den langfristigen Erfolg des Unternehmens zu sichern.