Ein Unternehmensverkauf bringt viele Herausforderungen mit sich – besonders in steuerlicher Hinsicht. Welche Steuern fallen an? Wie beeinflusst die Rechtsform die Steuerbelastung? Und welche Strategien helfen, den Verkaufsgewinn zu optimieren?

In diesem Beitrag erfahren Sie, worauf Sie bei den Steuern beim Unternehmensverkauf achten sollten und wie Sie durch eine gezielte Planung Ihre Steuerbelastung reduzieren. Da jede Transaktion individuell ist, empfiehlt sich eine frühzeitige Abstimmung mit Experten.

Basics webinar presented by Nils Koerber

Company sale (M&A) without risk and loss of value

Table of contents

The most important types of tax in business succession

Wenn Sie die Nachfolge Ihres Unternehmens planen oder einen Verkauf in Erwägung ziehen, sollten Sie sich mit den relevanten Steuerarten vertraut machen, die aufgrund Ihrer spezifischen Situation anfallen könnten. Zwei der wichtigsten Steuerarten, die in solchen Fällen eine Rolle spielen, sind die Income tax and the Inheritance or gift tax. Diese Steuern können erhebliche finanzielle Auswirkungen auf die Transaktion und die nachfolgende Vermögensverteilung haben.

Es ist entscheidend, dass Sie diese Steuerarten in Ihrer Planung berücksichtigen und frühzeitig mit einem erfahrenen Steuerberater oder einem spezialisierten Berater für Unternehmensnachfolgen zusammenarbeiten.

KERN has specialised in advising on the sale of companies in the SME sector since 2004. It was the first M&A consultancy to receive the GERMAN-BRAND-AWARD 2021 and was honoured by the SZ Institute as Best Consultant 2023.

Company sale & taxes: How the legal form determines your tax burden

Die gewählte Rechtsform eines Unternehmens hat nicht nur Auswirkungen auf Ihr Tagesgeschäft, sondern auch direkt auf die Unternehmensnachfolge. So unterscheidet man zwischen Einzel- und Mitunternehmern in Personengesellschaften und Gesellschaftern einer Kapitalgesellschaft.

Sole proprietors and co-entrepreneurs aber auch Unternehmer, die sich an Personengesellschaften beteiligen werden gleichsam versteuert. Zu diesen Personengesellschaften zählen auch Kommanditgesellschaften (KG beziehungsweise GmbH & Co. KG) sowie die offene Handelsgesellschaft (OHG). Und so wird ihr zu versteuernder Veräußerungsgewinn berechnet:

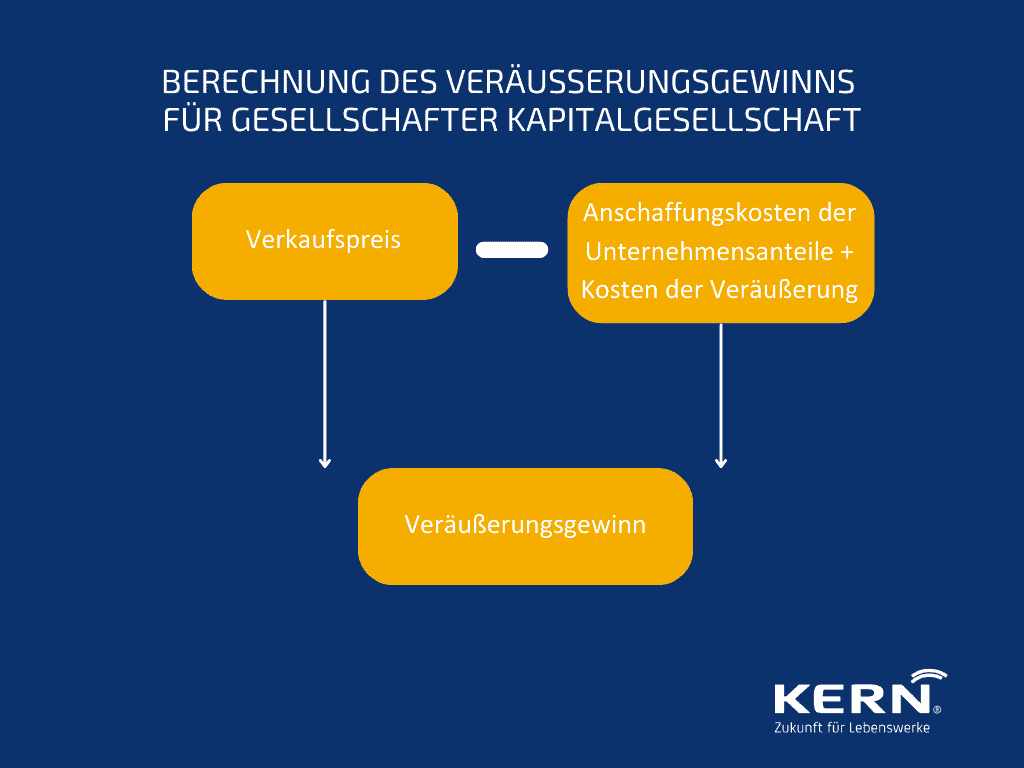

The shareholders of a Corporation unterliegen jedoch anderen Steuerregelungen da hier die Gesellschaftsanteile eines Unternehmens übertragen werden. Dabei werden vom Verkaufspreis die Anschaffungskosten der Unternehmensanteile sowie die Kosten der Veräußerung abgezogen. Hier lautet die Formel:

Taxes for internal succession

Noch vor wenigen Jahren ging die Mehrheit der deutsche Familienunternehmen an einen Nachfolger aus der Familie über an. Bei dieser Form der Nachfolge spielen Erbschaft- und Schenkungssteuern eine wesentliche Rolle. Hier gilt es zunächst zu klären, wer den Erbanspruch auf das Unternehmens hat, wer dieses Recht wahrnehmen möchte und welche steuerlichen Konsequenzen aus diesen Entscheidungen folgen. Dementsprechend können die folgenden Steuerarten anfallen:

Gift tax

The regulation of an inheritance and a succession are closely related from all perspectives. Because Not only company heirs are affected by inheritance and gift tax, sondern möglicherweise auch Käufer, die ein Unternehmen unter Marktwert erworben haben. Die Differenz zwischen Kaufpreis und Marktwert wird steuerlich als Schenkung betrachtet – die unter Umständen entsprechend versteuert werden muss.

Erbschafts- und Schenkungssteuern werden hierzulande auch im Gesetzbuch gemeinsam behandelt, da sie im steuerlichen Kontext miteinander vergleichbar sind. Die Regelungen zur Schenkung fungieren dabei in erster Linie als Ergänzung des Erbschaftsteuergesetzes. Durch sie soll verhindert werden, dass Erblasser und Erben die Erbschaftssteuer durch vorzeitige Schenkungen umgehen.

Aller zehn Jahre lassen sich im Rahmen einer Schenkung oder der vorweggenommenen Erbfolge lassen sich bereits zu Lebzeiten beträchtliche Vermögen steuerfrei an die nächste Generation übertragen. Der Freibetrag beträgt bei Erbschaften und Schenkungen beispielsweise bei leiblichen Kindern 400,000 euros per child. Auch Gesellschaftsanteile einer Firma können auf diesem Weg steuergünstig übertragen werden. Der Unternehmenswert sollte in diesem Fall auf jeden Fall über ein anerkanntes Verfahren wie dem IDW-S1 ermittelt werden. Auf Basis eines solchen objektivierten Gutachtens wird die Vermögensübertragung in den meisten Fällen vom Finanzamt akzeptiert.

Inheritance tax

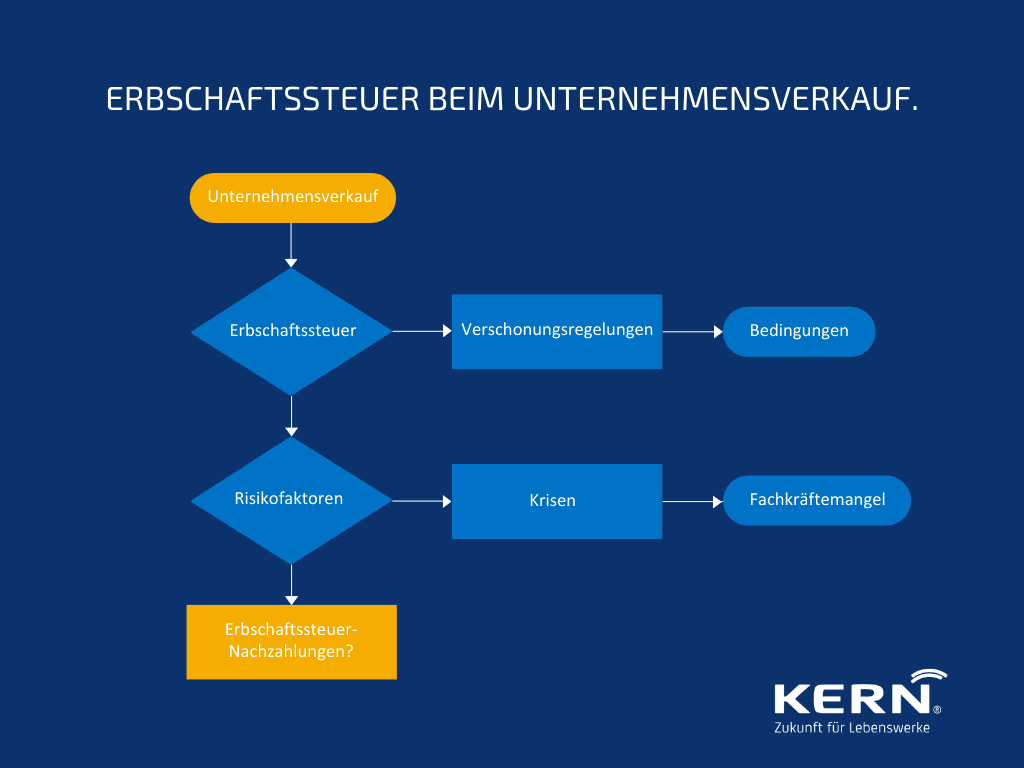

The Inheritance tax fällt beim Vermögensübergang von verstorbenen natürlichen Personen auf deren Erben an. Häufig stellt sie im familiengeführten Mittelstand bei der Vererbung von Betriebsvermögen eine große finanzielle Belastung dar, die die Weiterführung des Betriebes sogar ernsthaft gefährden kann. Der Gesetzgeber hat dieser Problematik bei seiner letzten großen Erbschaftsteuerreform Rechnung getragen und, wenngleich auch eingeschränkt, Ausnahmeregelungen für die Vererbung von Betriebsvermögen erlassen.

Soll die Schenkungs- oder Erbschaftssteuer nach der Übertragung auch aus dem Unternehmen finanziert werden, ist es ratsam die gängigen Verschonungs- und Begünstigungs Regelungen zu prüfen. Zu nennen wären hier:

- Retention scheme

- Standard exemption

- Option exemption

- Payroll regulation

- Meltdown of the standard and option exemption

- Besonderer Abschlag für familiengeführte Unternehmen

- Stundungsregelung in Todesfällen

Eine wesentliche Voraussetzung dieser Verschonungsregelung ist, dass die Lohnsumme bis zu 7 Jahre eine bestimmte Summe erreichen und das Unternehmen solange im Besitz der Erben sein muss. Damit ist die unternehmerische Freiheit unter Umständen für bis zu 7 Jahre stark eingegrenzt.

Beispielsweise führte die Corona-Pandemie viele Unternehmen in existenzbedrohende Situationen. Sie gingen in der Folge in Kurzarbeit oder bauten sogar Personal ab. In Zeiten des gleichzeitigen Fachkräftemangels nutzten viele Unternehmer diese Krisensituation ebenfalls für Investitionen in Produktivitäts Sprünge. Kurz: Aktuell ist nicht abzusehen, ob während der Krise oder danach noch ausreichend hohe Arbeitslöhne gezahlt werden, um die Payroll Prerequisites einzuhalten. Deshalb könnten in beiden Fällen Inheritance tax back payments the logical consequence be.

At this point we recommend the involvement of a transaction-experienced and specialised advisor. Since tax optimisation can quickly become very complex, good advice pays off quickly.

Combining succession planning with emergency preparedness

In der Praxis kommt es auch häufig vor, dass das Unternehmen nur an einen Erben übergeben werden soll oder ein Erbe das Unternehmen nicht erben möchte. Die Unterzeichnung einer Pflichtteilsverzichtserklärung or a Erbverzichtserklärung kann hier Abhilfe schaffen. Diese regelt den Verzicht auf Pflichtteilsansprüche des Erbens, der verzichtende Angehörige kann dann im Erbfall nicht mehr auf sein Pflichtteilsrecht bestehen. In der Nachfolgeplanung werden im Rahmen der Verzichtserklärungen häufig auch entsprechende Abfindungsregelungen mit den verzichtenden Erben vereinbart.

However, it becomes more complicated with an increasing number of successors. In this case, a (hopefully existing) Will zurückgegriffen werden. In der Regel wird im gleichen Zusammenhang auch noch die Versorgung des Ehepartners geklärt. Anders als bei der externen Nachfolge, geht es bei der familieninternen Nachfolge darum, eine vertragliche Lösung zu finden, die von der gesamten Familie mitgetragen wird. Die Testamente sollten dann auf jeden Fall mit den Gesellschaftsverträgen synchronisiert sein. Denn bei Abweichungen gelten immer die Regelungen der Gesellschaftsverträge.

Es ist anzuraten, die Nachfolgeplanung frühzeitig zu beginnen und mit der Notfallplanung zu verknüpfen. KERN bietet hierfür eine Structured emergency preparednesswhich answers the essential questions, structures the initial situation and is a good preparation for the succession plan.

Taxes in external succession

Aufgrund des Mangels an innerfamiliären Nachfolgern dominiert seit mehreren Jahren die externe Nachfolge, also der Company sale an Dritte. Analog zum familieninternen Generationswechsel können bei einer externen Nachfolge Income taxes, anfallen. Darüber hinaus sind in Abhängigkeit von der Transaktionsstruktur auch umsatzsteuerliche Konsequenzen zu beachten. Und, geht es um deutschen Grundbesitz, wird auch Real estate transfer tax fällig.

Für die externe Nachfolge ist es daher wichtig, bestimmte steuerliche Maßnahmen vor dem geplanten Verkauf einzuleiten. Der Gewinn beim Verkauf des Betriebes wird dabei grundsätzlich versteuert – also der Betrag, der den Buchwert ihres Unternehmens übersteigt.

Income tax

Bei jedem Unternehmensverkauf oder Anteilsverkauf werden Einkommensteuern fällig. Steuerrechtlich kommt es auf die Höhe des Veräußerungsgewinns – nicht zu verwechseln mit dem Veräußerungspreis – an. Er bildet die Besteuerungsgrundlage für die Berechnung der Einkommensteuer.

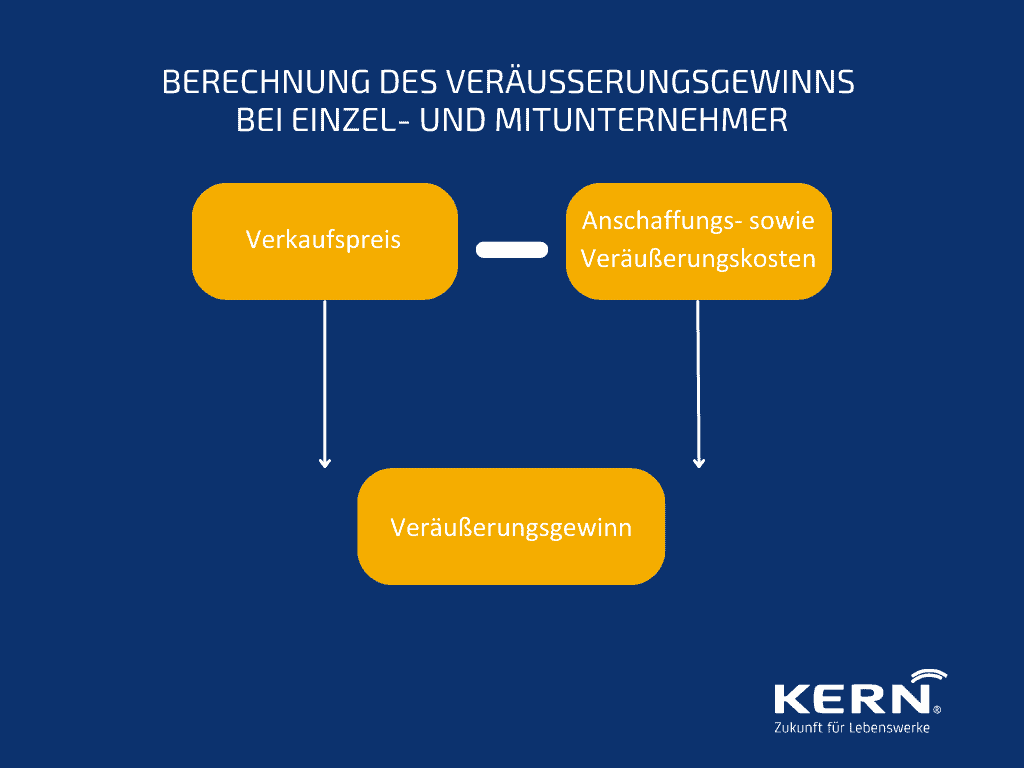

Der Veräußerungsgewinn berechnet sich bei Einzelunternehmen und Personengesellschaften wie folgt:

Der Veräußerungsgewinn zählt zu den Einkünften aus Gewerbebetrieb, unterliegt aber aufgrund seines durch ihn ausgelösten Progression Effektes steuerlichen Sonderregelungen, die nach § 34 EStG als außerordentliche Einkünfte behandelt werden.

| Veräußerungspreis |

| – Veräußerungskosten, z.B. Notargebühren, Consulting costs, commissions – Buchwert des Betriebsvermögens |

| = Veräußerungsgewinn |

Wie sich die Steuerlast je nach Veräußerungsform verändert

Verkauft ein Unternehmer Anteile an einer Kapital- oder Personengesellschaft, fallen grundsätzlich Einkommensteuer an. Liegen die Anteile an einer Kapitalgesellschaft im Betriebsvermögen des Unternehmers, sind nur 60% des Veräußerungsgewinns im Rahmen des Teileinkünfteverfahrens taxable in the form of income tax.

Beim Verkauf einer Kapitalgesellschaft bietet der Verkauf von Gesellschaftsanteilen (“Share deal”) grundsätzlich steuerliche Vorteile gegenüber dem Verkauf von Vermögensgegenständen (“Asset deal”). Aufgrund des Teileinkünfteverfahrens sind gemäß § 3 Abs. 40a EStG 40% des Veräußerungsgewinns steuerfrei.

Sollten sich die Anteile im Privatvermögen befinden, ist zu prüfen, ob eine so genannte wesentliche Beteiligung von mindestens 1 Prozent an der Kapitalgesellschaft vorliegt. In einem solchen Fall unterliegen die Gewinne ebenfalls dem Teileinkünfteverfahren. Liegt jedoch eine sogenannte Kleinstbeteiligung mit einem unter 1% vor, wird Abgeltungsteuer fällig (25% zuzüglich Solidaritätszuschlag und gegebenenfalls Kirchensteuer).

Tip: Wurde die Kleinstbeteiligung vor 2009 erworben, so ist deren Veräußerung steuerfrei.

Beim Verkauf einer (gewerblichen) Personengesellschaft ist aus steuerlicher Sicht grundsätzlich nicht entscheidend, ob die Personengesellschaft in Teilen oder als Ganzes verkauft wird. oder ob die Personengesellschaft ihre Wirtschaftsgüter veräußert. In beiden Fällen liegt ein „Asset Deal“ vor und der Veräußerungsgewinn ist in beiden Fällen steuerbar..

Tip: Die Veräußerung von ganzen Betrieben oder gesamten Mitunternehmeranteilen durch Privatpersonen kann unter anderem in Abhängigkeit von der Höhe des Veräußerungsgewinns und dem Alter des Verkäufers begünstigt werden. So kann der Übergeber eine Ermäßigung des Einkommensteuersatzes für Veräußerungsgewinne bis zu einer bestimmten Höhe nutzen. Gemäß § 34 Abs. 3 EStG kann auf Antrag einmal im Leben, wenn der Steuerpflichtige das 55. Lebensjahr beendet hat oder dauerhaft berufsunfähig ist, bis zu einem Betrag von insgesamt 5 Mio. € nach dem ermäßigten Steuersatz bemessen werden. Der ermäßigte Steuersatz beträgt in diesem Fall bis zu 56 % des durchschnittlichen Steuersatzes. Voraussetzung dafür ist eine Betriebsveräußerung im Ganzen.

Excursus: Difference between value and price

Wo liegt der Unterschied zwischen Wert und Preis und was wird tatsächlich besteuert?

Entscheidend für die Besteuerung ist der Unternehmenswert. Er wird mit wissenschaftlichen Methoden stichtagsbezogen auf Basis bestimmter Annahmen ermittelt. Er bringt zum Ausdruck was der Bewertende mit der Firma plant und ist von der gewählten Methode der Unternehmenswertberechnung abhängig. Hier erfahren Sie mehr, wie Sie Ihren Calculate enterprise value and which methods for Business valuation there is.

Entscheidend ist allerdings: Der errechnete Unternehmenswert ist immer unterschiedlich vom Marktwert. Der Marktwert hingegen wird im Rahmen einer Verhandlung erzielt, bei der es auf das Verhandlungsgeschick von Käufer und Verkäufer ankommt. Zudem beeinflussen viele unterschiedliche Faktoren den Marktwert einer Firma. Dies ist zunächst einmal Angebot und Nachfrage in einer bestimmten Branche, die allgemeinen Branchenentwicklung, die individuellen Entwicklung der zum Verkauf stehenden Firma und schließlich auch die zukünftigen Ertragserwartungen des Käufers.

Steueroptimierung für Käufer: Frühzeitig richtig planen

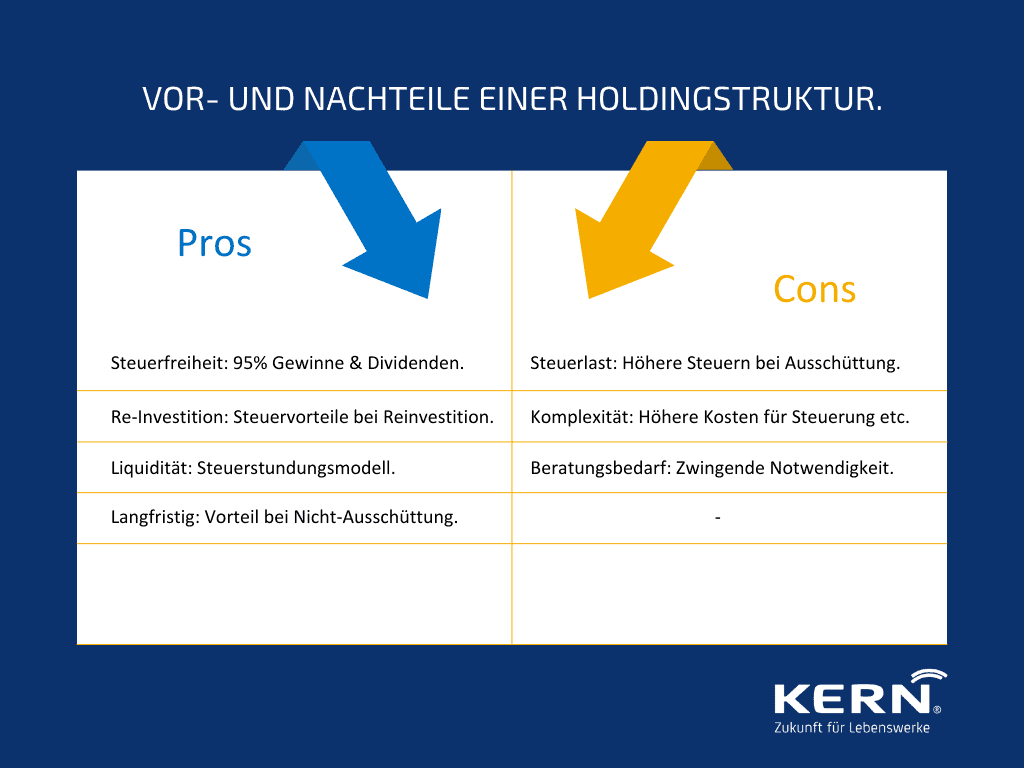

Steuervergünstigungen/ Holding

Hat ein Unternehmenskäufer die Absicht, sein Unternehmen oder seine Beteiligung mit einem Gesellschaftsanteil von mehr als 15% in einigen Jahren wieder zu verkaufen, ist eine Holding structure grundsätzlich dafür geeignet. Denn nach aktueller Rechtslage sind Veräußerungsgewinne und Dividenden auf Ebene der Holding zu 95% steuerbefreit.

Dies lohnt sich insbesondere für Unternehmer, die Erträge aus Unternehmensverkäufen beziehungsweise Beteiligungserträgen wieder in andere unternehmerische Aktivitäten re-investieren wollen. Diese Erträge verlassen bei einer Ausschüttung an die Gesellschafter immer die steuerbegünstigte Sphäre der Holding. In diesem Fall müssen die Gesellschafter mit einer geringfügig höheren Steuerlast als bei einer Direktbeteiligung am Unternehmen rechnen.

Dieses Modell ist jedoch eher ein Steuerstundungs- als ein Steuervermeidungsmodell, aus der sich ein Liquiditätsvorteil für den Unternehmer ergibt. Wird nicht ausgeschüttet kann dies einen sehr langfristigen Steuervorteil ergeben.

Und bei allem Willen zur steuerlichen Optimierung gilt für Familienunternehmer im Gegensatz zu Konzernen: Halten Sie Ihre Beteiligungsstruktur einfach. Denn je komplexer desto teurer wird die Steuerung. Stellen einer möglichen Steuerersparnis sind die Kosten für Beratung, Firmengründung, Buchführung und Jahresabschlüsse entgegen. Auch hier ist die Beratung durch einen Steuerberater zwingend zu empfehlen, damit sich die steuerlichen Vorteile, die eine Holdingstruktur bietet, auch realisieren lassen.

Was ist unter Anschaffungskosten bzw. Veräußerungskosten zu verstehen?

Die Anschaffungskosten einer Beteiligung sind gemäß §253 HGB höchstens in der tatsächlichen Höhe anzusetzen. Unabhängig davon, ob die Beteiligung Gewinne oder Verluste erwirtschaftet, bleiben die Anschaffungskosten grundsätzlich unverändert.

Beim Erwerb oder Verkauf eines Unternehmens fallen grundsätzlich auch Nebenkosten an. Dazu zählen u.a. auch Beratungsaufwendungen, Provisionen, Aufwände für Sachverständige sowie Notargebühren. Diese Anschaffungskosten können vom Veräußerungserlös ebenso wie die Veräußerungskosten abgezogen werden, so dass sich der zu versteuernde Veräußerungsgewinn verringert.

When is a company sale tax-free?

Steuerfrei ist ein Unternehmensverkauf nur bei kleinen Firmen, die einen Veräußerungsgewinn von bis zu 45.000 Euro erzielen.

Der Gesetzgeber hat diesen Freibetrag bei Betriebsveräußerungen vorgesehen wenn der Unternehmer bereits das 55. Lebensjahr vollendet hat der auf die Veräußerungsgewinne anzuwenden ist (§ 16 Abs. 4 EStG ).

Conditions:

- Dieser Freibetrag kann nur einmal im Leben in Anspruch genommen (“Ein-Mal-im-Leben-Regelung”) werden und beläuft sich auf 45.000€

- Dieser Freibetrag verringert sich, sobald der Veräußerungsgewinn 136.000€ (Freigrenze) übersteigt.

Das heißt: Übersteigt der Veräußerungsgewinn 181.000€ hat der Verkäufer keinen konkreten Vorteil mehr von dem Freibetrag. Der steuerpflichtige Veräußerungsgewinn ist dementsprechend gleich zum Veräußerungsgewinn.

Deshalb ist der hohe, einmalige Freibetrag bei Unternehmensveräußerungen für Unternehmer mit vollendetem 55. Lebensjahr primär bei kleinerer Unternehmensgröße und entsprechendem geringeren Unternehmens Verkaufspreis relevant.

Reducing taxes when selling a business: The role of planning and timing

Zeit ist bei der Vorbereitung eines Unternehmensverkaufs ein wichtiger Faktor. Denn je früher für Sie Klarheit zu möglichen Übergabe Szenarien besteht, desto eher können Sie innerhalb der gesetzlichen Fristen Vorsorge für ein optimales Ergebnis treffen. Bitte behalten Sie im Hinterkopf: Die steuerliche Optimierung benötigt insbesondere im Hinblick auf die Nachfolge Zeit, Wirkung zu entfalten. Beraten Sie sich mit einem transaktionserfahrenen Nachfolgespezialisten, mit dem Sie einen professionellen M&A process prepare. Together with your advisor, you plan your company sale, take a tax burden comparison based on this and identify tax optimisation potential.

An dieser Stelle möchten wir darauf hinweisen, dass es sich gerade in Vorbereitung eines geplanten Unternehmensverkaufes lohnt, Ertragssteuern zu zahlen. Im Rahmen eines Fitness checks können Sie weitere Wertsteigerungspotenziale heben und diese in einer Balance sheet adjustment make visible. This, too, is not done overnight: On average, the entire Company sale procedure zwischen zwei und fünf Jahren. Und diese Strategie lohnt sich. Denn die sichtbar gemachten Erträge machen Unternehmen attraktiver und verbessern die Chancen für einen erfolgreichen Verkauf. Positiver Nebeneffekt: Die Ertragsteuern sind eine gute Investition.

Ein kleines Rechenbeispiel: Eine Ertragssteigerung um 25% zeigt in der Praxis einen oft überdurchschnittlichen Anstieg in der Calculation of the enterprise value and thus the achievable purchase price. Against this background, some tax-saving models that are popular among small and medium-sized enterprises quickly become relative.

Conclusion

Beginnen Sie rechtzeitig mit der Planung Ihrer Unternehmensnachfolge. Treffen Sie ihre individuelle Entscheidung, ob Sie eine interne oder eine externe Unternehmensnachfolge bevorzugen. Ihre Antwort auf diese Frage schafft wiederum Klarheit, welche der verschiedenen Steuerarten für Ihren Übergabeprozess Relevanz besitzen.

Und last but not least eröffnet sich bei einer rechtzeitigen Vorbereitung ihrer Nachfolge die Möglichkeit, Vorteile aus den verschiedenen Steuervergünstigungen ziehen und somit Steuern zu “sparen”.

Häufige Fragen

How is a company sale taxed?

Ein Unternehmensverkauf wir immer auf Basis des Ertrags, d.h. dem Brutto-Verkaufserlös abzüglich von Anschaffungskosten und Nebenkosten des Verkaufs besteuert. Die Höhe der Steuerlast richtet sich danach, ob der Veräußerer eine natürliche oder juristische Person (z.B. in Form einer Holdinggesellschaft) ist.

Like a Company sale to succeed in 10 steps, you can find out in our KERN expert video.

How is the sale of a GmbH taxed?

Share Deal vs. Asset Deal: If you have a Sell limited liability company möchten, ist der Verkauf durch das sogenannte Teileinkünfteverfahren zu 40% steuerfrei. Bei Holdinggesellschaften gibt es sogar eine Steuerbefreiung von 95% während die verbleibenden 5% wiederum nach dem Teileinkünfteverfahren besteuert werden. Sell GmbH Taxes: Der Verkauf von GmbH-Anteilen im Rahmen eines “Share Deals” ist damit für den Verkäufer steuerlich oft vorteilhafter als der Verkauf der einzelnen Wirtschaftsgüter im Rahmen eines “Asset-Deals”.

Wie hoch wird der Veräußerungsgewinn versteuert?

Dies hängt davon ab, ob der Verkäufer eine natürliche Person oder eine juristische Person (z.B. eine GmbH oder AG) ist. Unternehmensverkäufe durch natürliche Personen werden abhängig von deren individuellen steuerlichen Situation zunächst auf der Basis des persönlichen Steuersatzes besteuert. Es gibt jedoch eine ganze Reihe von Steuervergünstigungen und Freibeträgen, deren Nutzung im Gespräch mit einem Steuerberater zu prüfen ist. Unternehmensverkäufe von Kapitalgesellschaften werden zunächst im Rahmen des Teileinkünfteverfahrens besteuert. Auch hier ermöglicht der Gesetzgeber in bestimmten Konstellationen eine weitgehende Steuer Verschonung, so dass die Gesamtsteuerbelastung auf bis zu 1,5% reduziert werden kann.

Rechenmodell ab 55 Jahren – halber Steuersatz

Angenommen, Sie sind 64 Jahre alt und Bäckermeister. 2021 haben Sie Ihre Bäckerei mit einem Veräußerungsgewinn von 130.000 Euro verkauft. In dem Jahr machte Ihr Betrieb vor der Veräußerung noch einen Gewinn von 40.000 Euro. Anträge für den ermäßigten Steuersatz oder den Freibetrag haben Sie bisher nicht gestellt. Sie habenalso Ihr 55. Lebensjahr vollendet und Ihren Betrieb mit einem Gewinn von nicht mehr als fünf Millionen Euro veräußert. Sie dürfen mithin sowohl den ermäßigten Steuersatz als auch den Freibetrag in Anspruch nehmen. Der ermäßigte Steuersatz ist für Sie als steuerpflichtiger Unternehmer in der Regel vorteilhafter. Ihre Berechnungen könnten wie folgt aussehen:

- Veräußerungsgewinn 120.000 € – Freibetrag 45.000 €

- = steuerpflichtiger Veräußerungsgewinn 75.000 €

- steuerpflichtiger Veräußerungsgewinn 75.000 € + laufender Gewinn 30.000 €

- = Gesamtbetrag der Einkünfte 105.000 €

- Die normale Einkommensteuer beträgt bei einem durchschnittlichen Steuersatz von 35,22 % 36.981 €.

- Im Falle eines Betriebs Verkaufs reduziert sich die Einkommensteuer für den Veräußerungsgewinn auf von 35,22% auf 19,72% (35,22% x 56%)

- Somit schulden Sie dem Finanzamt für Ihren Veräußerungsgewinn 14.790 Euro und für Ihren Gewinn 10.566 €.

- Ihre Steuervergünstigung beträgt somit 11.625 €